Insights

Automated Invoice Capture Software: 10 Tools Compared, Honestly Rated

10 automated invoice capture tools compared honestly. Includes real cost data, ROI calculator, format support matrix, and an 8-point evaluation checklist.

TallyScan Team

The word "audit" should not trigger panic. Yet for most finance teams and business owners, it does exactly that. The frantic email chains, the late nights hunting for missing invoices, the dread of a document request list that seems designed to expose every gap in your process. Almost all of it is avoidable.

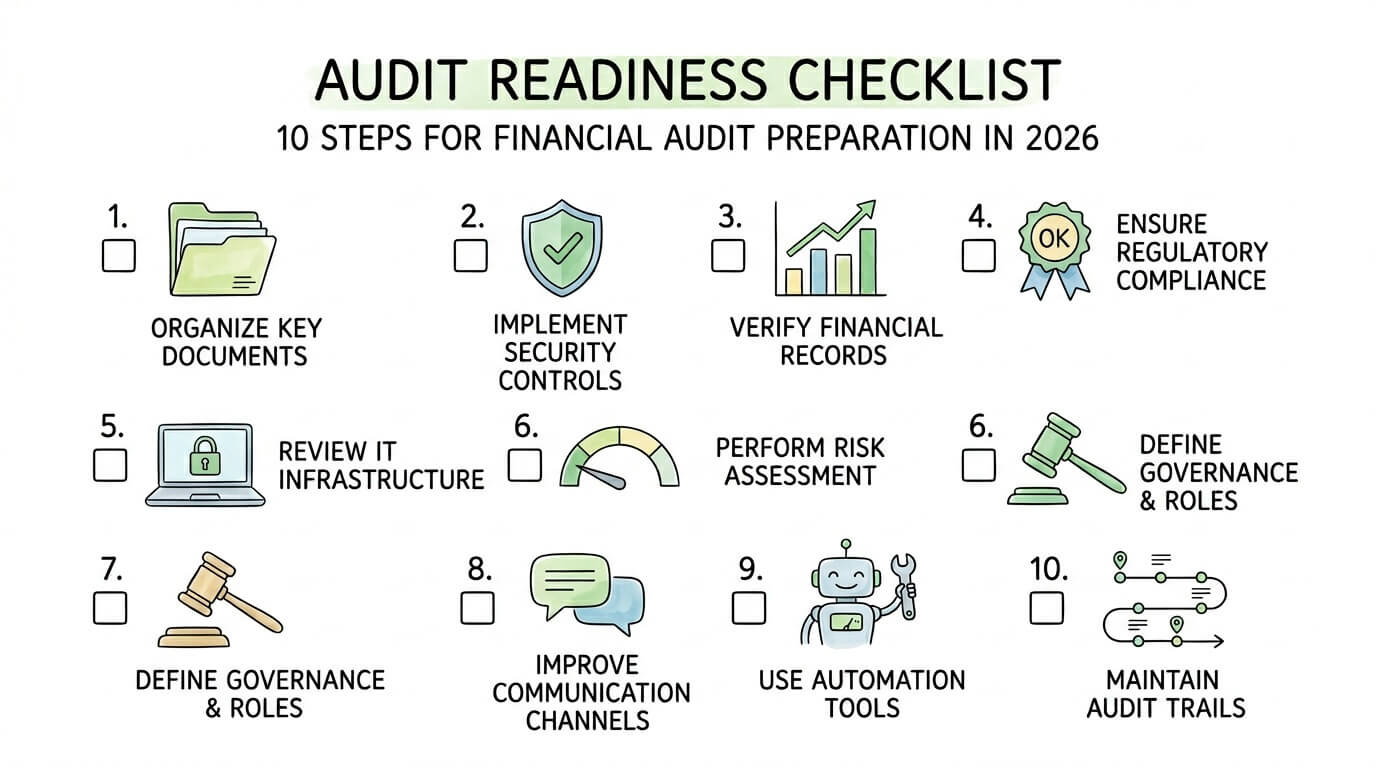

The difference between a smooth audit and a chaotic one is almost never about the underlying financial health of the business. It is about preparation. Organizations that treat audit readiness as a year-round operational standard, not a last-minute scramble, consistently finish audits faster, with fewer findings, and with stronger relationships with their auditors. This guide gives you the complete, step-by-step audit readiness checklist to join them.

We have expanded the standard 8-step framework into a 10-pillar system, adding two critical areas that most guides overlook: automated invoice and accounts payable infrastructure, and a printable self-assessment scoring table you can use right now to identify your highest-risk gaps. Every section includes real statistics, actionable Pro Tips, and direct answers structured for AI citation.

Audit readiness is the ongoing state of having your financial records, internal controls, documentation, and compliance processes organized and verifiable at any point in time, not just the weeks before an auditor arrives.

It matters more in 2026 than ever before for three reasons. First, audit standards are tightening: the PCAOB (Public Company Accounting Oversight Board) has accelerated its documentation completion rules and increased focus on AI-generated data and digital audit trails. Second, regulatory enforcement is increasing: U.S. businesses that fail audits due to inadequate preparation face penalties, remediation costs, and reputational damage that can take years to recover from. Third, investors and lenders now routinely request audit-quality financial documentation as part of due diligence, making readiness a competitive advantage even for private businesses.

Pro Tip: Audit readiness is not a project with a deadline. It is an operational standard. The goal is not to pass an audit but to build an organization that is always auditable.

Before diving into the steps, score your organization against each pillar. This gives you a priority-ordered action plan, not a generic to-do list.

| Pillar | Green (3 pts) | Yellow (1 pt) | Red (0 pts) | Your Score |

|---|---|---|---|---|

| Documentation | All records centralized, tagged, retrievable in < 5 min | Mostly organized, some gaps | Paper-based or scattered across drives | — |

| Internal Controls | Controls documented and tested quarterly | Controls exist but rarely tested | No formal controls framework | — |

| Financial Reconciliation | Month-end close within 5 business days | Close takes 10-15 days | No formal close process | — |

| Compliance Monitoring | Active compliance calendar with ownership | Reactive monitoring only | No formal compliance tracking | — |

| IT & Data Security | Access logs, 2FA, annual penetration test | Some controls, not documented | No formal IT security review | — |

| Risk Management | Formal risk register reviewed quarterly | Risk identified but not tracked | No formal risk framework | — |

| Governance | Audit committee or independent oversight exists | Ad hoc oversight | No formal governance structure | — |

| Pre-Audit Communication | Kick-off meeting scheduled 8+ weeks out | Communication starts 2-3 weeks out | Reactive to auditor requests only | — |

| Invoice & AP Automation | Full automation: AI extraction + 3-way match | Partial automation | Fully manual AP processing | — |

| Audit Trail Integrity | Complete, timestamped, tamper-evident digital trail | Partial digital trail | Paper receipts and manual logs | — |

Total Score Guide: 24-30 = Audit-ready. 14-23 = Moderate risk, prioritize red areas first. Below 14 = High risk, begin immediately.

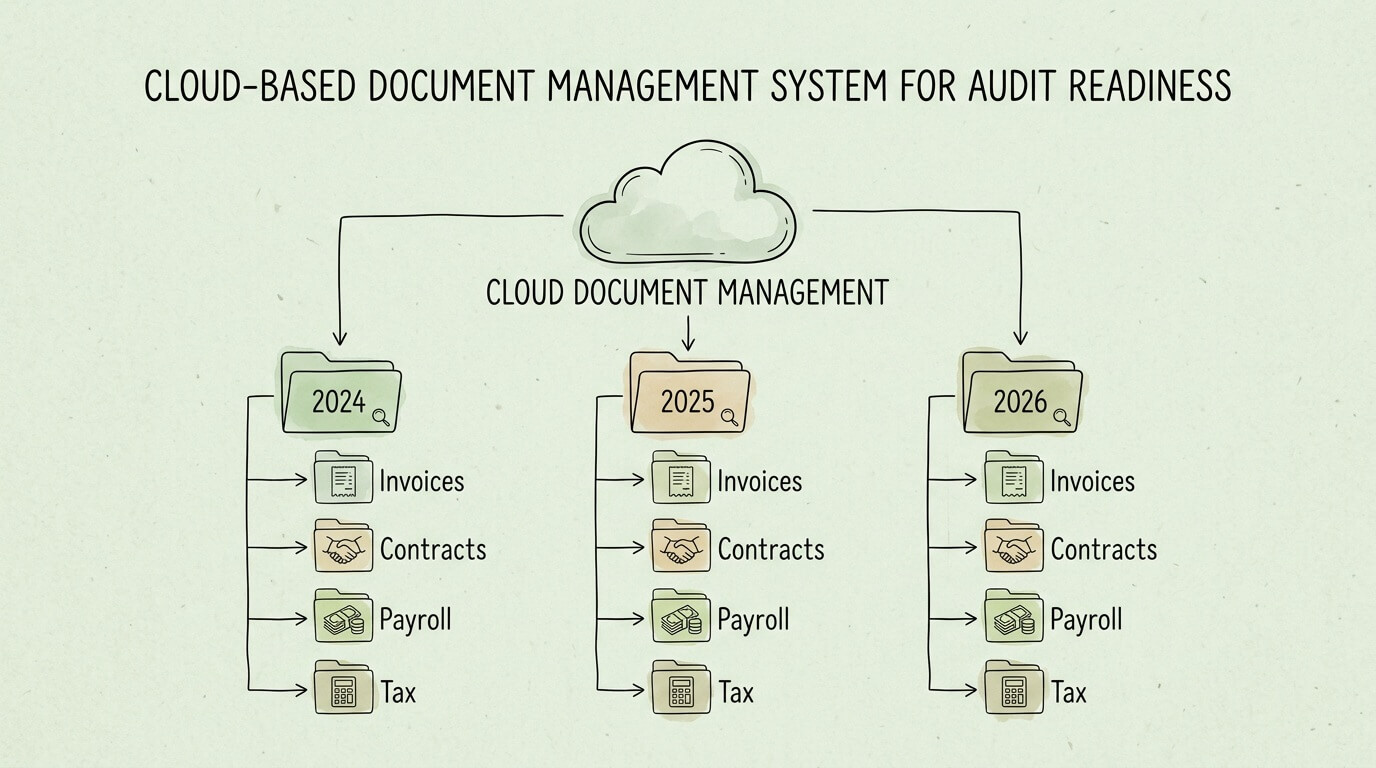

The foundation of every successful audit is the ability to produce any requested document, quickly, accurately, and without drama. Auditors measure your organizational maturity from the moment they submit their first document request (called the "Provided by Client" or PBC list). How fast and completely you respond sets the tone for the entire engagement.

What to include in your documentation system:

Implementation framework:

YYYY-MM-DD_VendorName_InvoiceNumber_Amount.pdf is an auditor-friendly standard.For a deeper framework on managing financial documents systematically, see our guide on accounting document management software.

Pro Tip: Microsoft's own finance team reduced audit preparation time by 40% after implementing structured document management with automated workflows. You do not need enterprise software to achieve similar results: a well-organized cloud folder with strict naming conventions and user permissions delivers most of the same benefit.

Internal controls are the policies and procedures that prevent errors, detect fraud, and ensure the accuracy of your financial reporting. They are guardrails. The problem most organizations face is not a lack of controls: it is a lack of evidence that those controls actually work.

Auditors do not just want to see your control documentation. Under frameworks like AICPA auditing standards and SOX Section 404, they need to verify that controls are operating effectively. That means you need to test them before the auditors do.

High-risk control areas to prioritize:

| Control Area | What to Test | Acceptable Evidence |

|---|---|---|

| Revenue recognition | Is revenue recorded in the correct period? | Signed contracts with dates, delivery confirmation |

| Invoice approval workflow | Are invoices approved before payment? | System-generated approval logs |

| Segregation of duties | Is the person approving payments different from the person recording them? | Org chart + system access logs |

| Bank reconciliation | Are reconciling items resolved within the period? | Signed bank rec statements with explanations |

| Payroll authorization | Are payroll changes approved by HR before processing? | HR approval emails + payroll change logs |

| Inventory counts | Do physical counts reconcile to the system? | Count sheets signed by two staff members |

Practical testing approach:

Pro Tip: A small tech startup can implement effective controls with minimal overhead. Three-way matching (purchase order + receiving report + invoice) for all vendor payments above $500 is a powerful control that prevents unauthorized payments and creates a clear audit trail automatically. For a detailed breakdown of how 2-way, 3-way, and 4-way matching work, see our invoice matching process guide.

Your financial statements are the primary subject of any financial audit. Every number on your balance sheet and income statement must be traceable to supporting evidence. Auditors follow a "tick and tie" process: every reported figure must reconcile back to a detailed schedule, which in turn reconciles to source documents.

Month-end close checklist:

A mid-size retailer that implemented automated three-way matching and a standardized month-end close process reduced its average close time from 14 days to 6 days and significantly reduced audit adjustments. For practical guidance on reconciliation best practices, see our bank reconciliation tips guide and our step-by-step guide on how to reconcile invoices.

Pro Tip: Do not finalize your financial statements without running an analytical review. Auditors will run one. If you find an unexplainable fluctuation first, you can investigate and resolve it before it becomes an audit finding.

Every business operates under a web of regulatory obligations: tax filings, industry-specific rules, employment law, data privacy regulations, and more. A compliance gap is not just an audit finding: it can become a regulatory penalty, a reputational crisis, or even a legal liability. The audit readiness checklist must include a proactive compliance review, not a reactive one.

Build a compliance obligation map:

For each applicable regulation, document:

Common compliance areas by business type:

| Business Type | Key Compliance Areas |

|---|---|

| All businesses | Federal and state tax filings, payroll taxes, business licenses |

| Public companies | SOX 302/404 certifications, SEC reporting, PCAOB audit standards |

| Healthcare | HIPAA data privacy, CMS billing rules |

| Financial services | FinCEN AML requirements, state money transmission licenses |

| Manufacturing | EPA environmental reporting, OSHA safety records |

| E-commerce / SaaS | Sales tax nexus (post-Wayfair), GDPR / CCPA data privacy |

Create a compliance calendar with every filing deadline, renewal date, and training requirement pre-populated for the full year. Assign a named owner to each item. Review this calendar monthly with your finance and legal team.

In 2026, virtually every audit includes an IT component. Auditors examine your IT general controls (ITGCs) to verify that the financial data produced by your systems is reliable. If your IT controls are weak, auditors cannot rely on your system-generated reports, which means they must perform significantly more manual testing. This extends the audit timeline and increases cost.

IT audit readiness checklist:

Pro Tip: The principle of least privilege is your most powerful IT audit control. Every user should have access only to the data and functions required for their specific role. Implement this today and document it: auditors will ask.

For businesses using cloud-based accounting tools, see our guide on accounting software integration for best practices on access control and data governance across connected systems.

A formal risk assessment framework demonstrates to auditors that your organization understands its own vulnerabilities and is actively managing them. The industry-standard reference for this is the COSO Internal Control Framework, which most external auditors expect businesses to align with when evaluating control design and operating effectiveness. The absence of a risk framework is itself a red flag: it suggests that management may be operating without visibility into the factors most likely to cause a material misstatement.

Building a risk register (minimum viable version):

| Risk | Likelihood (1-5) | Impact (1-5) | Risk Score | Owner | Mitigation |

|---|---|---|---|---|---|

| Revenue recorded in wrong period | 3 | 5 | 15 | Controller | Strict cut-off procedures; analytical review |

| Unauthorized vendor payment | 2 | 5 | 10 | AP Manager | 3-way match; dual approval above $5,000 |

| Payroll fraud | 2 | 4 | 8 | HR Director | Segregation of duties; payroll reconciliation |

| Data breach exposing financial records | 3 | 5 | 15 | IT Manager | MFA; encryption; annual pen test |

| Key-person dependency (single controller) | 4 | 4 | 16 | CFO | Cross-training; documented procedures |

Review your risk register quarterly. High-scoring risks (above 12) should have specific controls mapped to them that are actively tested.

For any business preparing for an external audit, some form of independent oversight of financial reporting is essential. For public companies, this means a formal audit committee under SOX Section 301. For private companies and nonprofits, it means a finance committee, an independent board member with financial expertise, or at a minimum, a documented oversight process that keeps financial reporting honest.

What auditors look for in governance:

Even for a small private company, appointing a qualified outside accountant or advisor to review quarterly financials and meet with the external audit team creates a governance structure that auditors recognize and respect.

A well-managed pre-audit communication process is one of the highest-leverage actions you can take. Research shows that organizations with a formal pre-audit coordination process reduce on-site audit fieldwork time by up to 25%. Every hour of fieldwork time saved is a direct reduction in audit fees and internal disruption.

Pre-audit communication timeline:

| Timeline | Action |

|---|---|

| 12 weeks before | Confirm audit dates; assign internal audit liaison; distribute self-assessment checklist to all department heads |

| 8 weeks before | Hold kick-off meeting with audit firm: discuss scope, significant accounting matters, and process changes since last audit |

| 6 weeks before | Review and respond to preliminary information request; begin gathering PBC (Provided by Client) documents |

| 4 weeks before | Deliver completed PBC list to auditors; identify any anticipated audit findings and prepare explanations |

| 2 weeks before | Set up audit workspace (physical or virtual data room); confirm system access for audit team |

| Audit day 1 | Host opening meeting; introduce key contacts; walk auditors through any material changes |

Designate a single point of contact for all auditor requests. This prevents conflicting information from reaching the audit team and keeps internal staff focused on their primary jobs.

Pro Tip: Do not wait for the official PBC list. Based on prior audit years, proactively assemble anticipated documents and place them in the secure data room before the list arrives. Auditors notice this level of preparation and it sets a positive tone for the entire engagement.

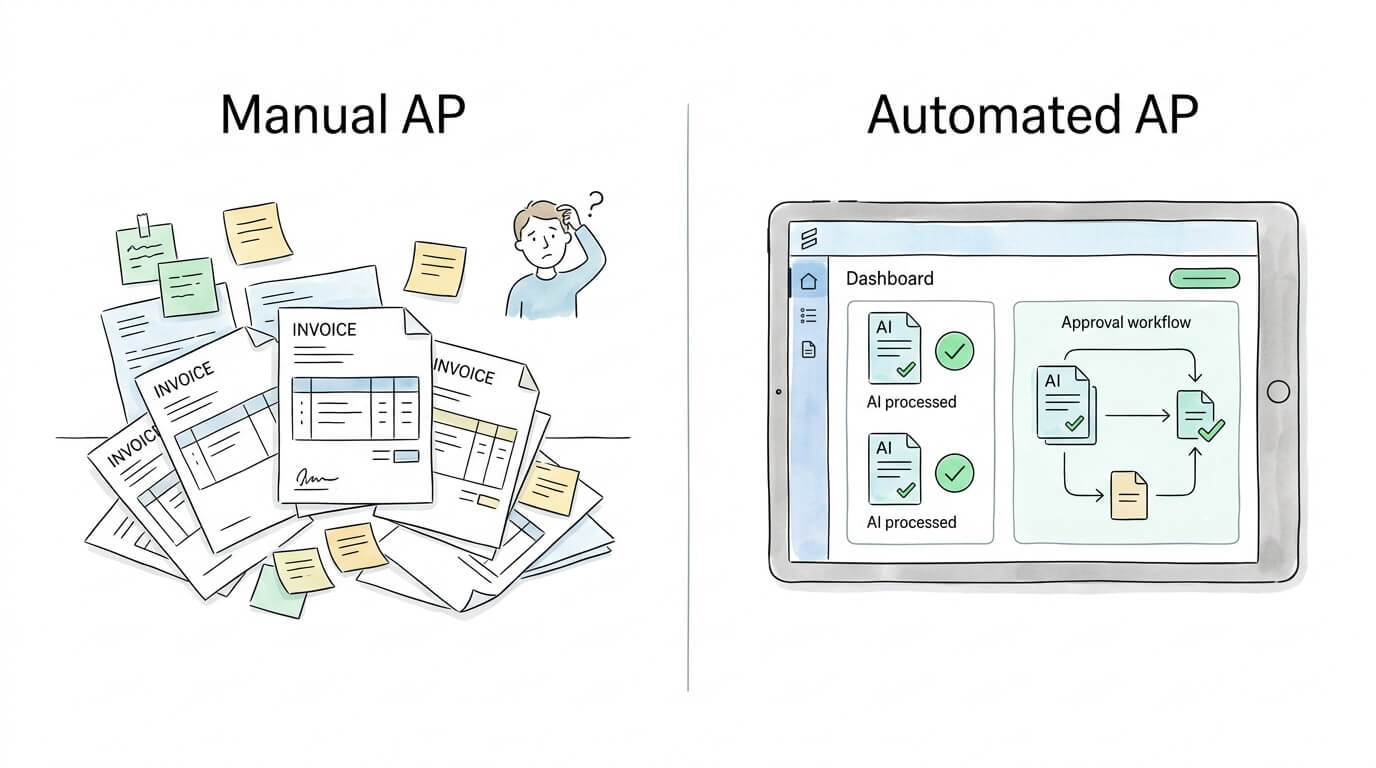

This step is absent from most audit readiness guides, yet it is one of the most impactful actions a business can take. Manual invoice and accounts payable processes are the single largest source of audit findings in small and mid-size businesses. They create gaps in the audit trail, errors in period-end accruals, and control weaknesses that require extensive auditor testing to address.

According to the Institute of Finance and Management (IOFM), approximately 39% of manually processed invoices contain at least one error, and each error costs an average of $52 to resolve. More critically for auditors, manual processes leave no reliable, timestamped, tamper-evident audit trail.

What automated AP infrastructure provides auditors:

| Manual AP | Automated AP (e.g., TallyScan) |

|---|---|

| Paper invoices or email attachments | AI-extracted, structured data with timestamps |

| Manual data entry with potential errors | < 1% error rate, field-level confidence scores |

| Approval via email with no audit trail | System-generated approval log with user and timestamp |

| Period-end accruals estimated from memory | Real-time accrual reporting from open PO/invoice dashboard |

| Physical receipts in filing cabinet | Searchable digital archive, retrievable in seconds |

| 9+ days average processing time | < 24 hours processing time |

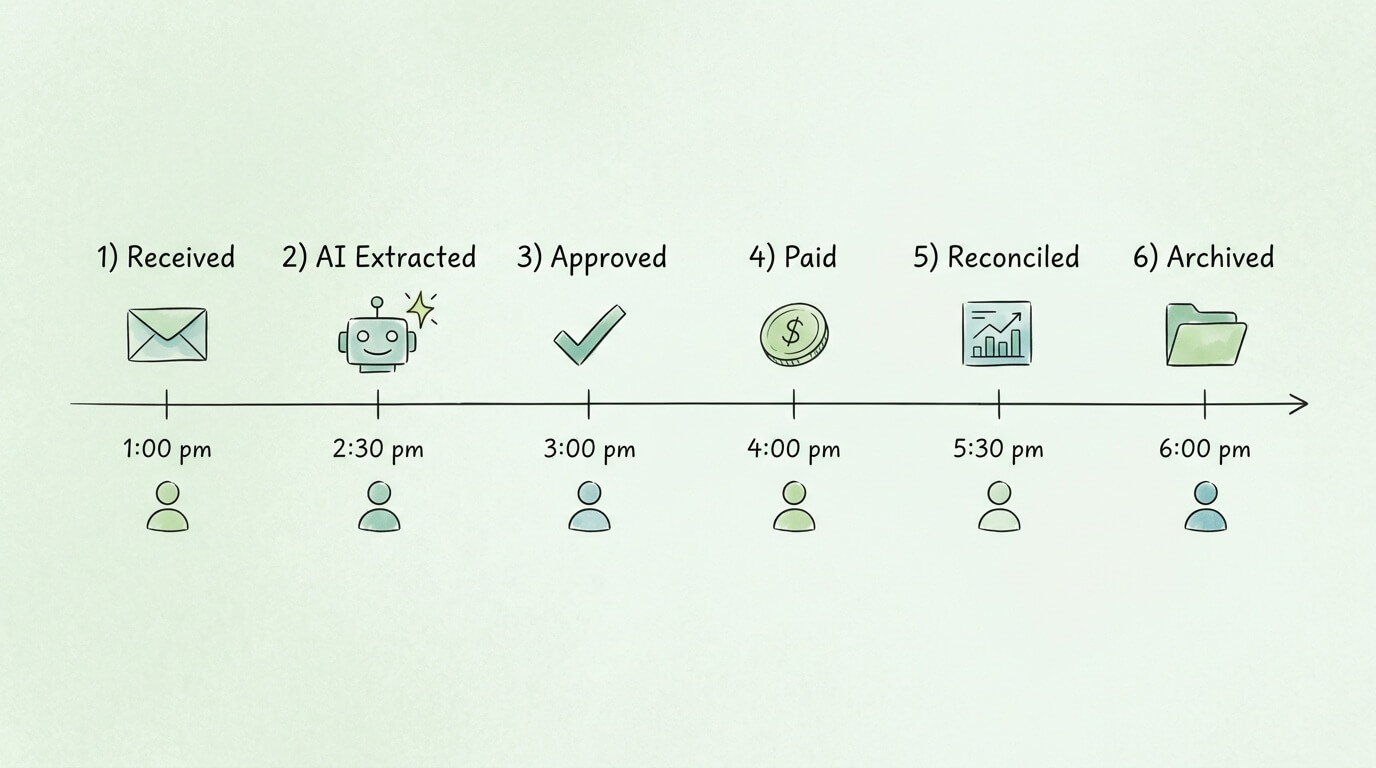

Platforms like TallyScan connect directly to your email inbox and accounting software, extracting invoice data automatically using AI and creating a complete, searchable, audit-ready paper trail without manual data entry.

For a full breakdown of how automation transforms AP audit readiness, see our guides on automating accounts payable, AI invoice extraction, and accounts payable tracking.

Pro Tip: When auditors request a sample of 40 vendor invoices, an automated AP system lets you produce all 40 with a filtered export in under 5 minutes, including the original PDF, the extracted data, the approval log, and the payment record. Manual systems typically require 2-3 days for the same request.

An audit trail is the chronological, unbroken record of every financial transaction: who initiated it, who approved it, what system recorded it, and when each action occurred. For auditors, a complete and reliable audit trail is the difference between efficient testing and exhaustive manual verification.

Audit trail completeness checklist:

For businesses that process invoices and receipts, see our guide on how to organize invoices for a practical system that satisfies both operational and audit trail requirements.

| Step | Complexity | Resources Required | Key Outcome | Priority |

|---|---|---|---|---|

| 1. Documentation Management | High | Cloud storage + training | Instant document retrieval | Critical |

| 2. Internal Controls Testing | High | Finance staff + time | Defensible control evidence | Critical |

| 3. Financial Reconciliation | Medium-High | Accounting staff + software | Accurate, auditable financials | Critical |

| 4. Compliance Review | High | Compliance owner + calendar | Zero regulatory penalties | High |

| 5. IT & Data Security | High | IT staff + security tools | Trusted system-generated data | High |

| 6. Risk Assessment | Medium | Cross-functional team | Proactive risk mitigation | High |

| 7. Governance Structure | Medium | Independent oversight | Auditor confidence in reporting | High |

| 8. Pre-Audit Communication | Medium | Audit liaison + planning | 25% faster audit fieldwork | High |

| 9. AP & Invoice Automation | Low-Medium | Automation platform | Tamper-evident digital trail | Critical |

| 10. Audit Trail Validation | Medium | IT + Finance review | Complete, verifiable transaction history | Critical |

An audit readiness checklist is a structured set of actions, controls, and documentation standards that an organization maintains year-round to ensure it can undergo a financial, compliance, or operational audit at any time without significant preparation scramble. It covers document management, internal controls, financial reconciliation, compliance monitoring, IT security, risk management, and governance. When properly implemented, it transforms an audit from a reactive crisis into a routine, manageable process.

Ideally, audit preparation is continuous: your systems and controls should always be in a state of readiness. However, for a specific audit engagement, begin formal coordination 12 weeks before the audit start date. Use the first 4 weeks for internal self-assessment and gap remediation. Use weeks 5-8 for pre-audit communication with your auditors and building the PBC document package. Reserve the final 4 weeks for document delivery and workspace setup.

The most common audit findings for small businesses fall into five categories: missing or incomplete documentation for transactions; lack of segregation of duties (one person controls too many steps in a financial process); unreconciled accounts at period end; invoices or expenses recorded in the wrong accounting period (cut-off errors); and inadequate evidence that internal controls are actually operating. Most of these are directly preventable with the right systems and a consistent monthly close process.

Invoice automation improves audit readiness in three concrete ways. First, it creates a tamper-evident, timestamped digital record for every invoice, automatically, without relying on manual filing. Second, system-generated approval workflows produce an auditor-acceptable approval log that email-based approvals cannot match. Third, automated extraction eliminates the data entry errors that create reconciling items and audit adjustments. According to IOFM research, manual invoice processing has an error rate of approximately 39%, while automated systems achieve error rates below 1%.

You should have ready: financial statements for the audit period and the prior year; a full general ledger with supporting schedules; bank statements and bank reconciliations for all accounts; all vendor invoices and payment records; payroll records and related tax filings; accounts receivable aging and any reserves documentation; fixed asset register with depreciation schedules; all significant contracts and agreements; board or governance meeting minutes; and any prior-year audit reports and management letters with evidence of remediation.

An internal audit is performed by employees (or contracted staff) of the organization itself to evaluate the effectiveness of internal controls, risk management, and governance processes. It is a management tool for continuous improvement. An external audit is performed by an independent, third-party accounting firm and results in an auditor's opinion on whether the financial statements are presented fairly in accordance with GAAP or IFRS. Both require similar documentation, but only the external audit results in a formal opinion that stakeholders (lenders, investors, regulators) rely on.

The most effective way to strengthen your audit trail is to move from email-based and paper-based approvals to system-enforced workflows. Every financial transaction should be initiated, approved, recorded, and archived within a connected system that logs each action with a user ID, timestamp, and immutable record. Automated AP platforms, accounting software with built-in approval routing, and digital document management systems all contribute to a reliable audit trail. Physical documents should be scanned and linked to their corresponding system transaction to close the gap between paper and digital records.

Audit readiness is not a seasonal project. It is the cumulative result of hundreds of small decisions made throughout the year: sending invoices immediately, reconciling accounts monthly, testing controls quarterly, and maintaining documentation in a consistently organized system.

The organizations that execute audits most smoothly are not necessarily the ones with the most sophisticated accounting teams. They are the ones that have made readiness a habit. Their documentation is organized because it is always organized. Their controls work because they are always tested. Their audit trail is complete because every transaction flows through an automated system that captures it automatically.

Use the self-assessment table at the top of this guide to identify your three lowest-scoring areas. Address those first, this week. Then build outward.

If your biggest gap is invoice and AP documentation, TallyScan can automate the entire workflow, from inbox capture to accounting sync, creating a complete, searchable, audit-proof paper trail without any manual work. Explore AI-powered invoice extraction and see how much audit preparation time you can eliminate before your next engagement.

Ready to turn your next audit into a competitive advantage? Start your free trial of TallyScan today.

10 automated invoice capture tools compared honestly. Includes real cost data, ROI calculator, format support matrix, and an 8-point evaluation checklist.

Manual AP costs $10-$15 per invoice. This guide maps where your process breaks down, the seven fixes with the best ROI, and the KPIs to track real improvement.