Insights

Automated Invoice Capture Software: 10 Tools Compared, Honestly Rated

10 automated invoice capture tools compared honestly. Includes real cost data, ROI calculator, format support matrix, and an 8-point evaluation checklist.

TallyScan Team

Cash flow is the single most important number on your business scorecard, yet it is also the most misunderstood. According to a U.S. Bank study, 82% of small businesses that fail cite cash flow problems as a contributing factor, not a lack of profit, not a bad product, and not a weak team. Cash.

The good news? Improving your cash flow is not a mystery. It comes down to three levers: collecting money faster, spending money smarter, and planning for what is coming. Pull all three, and you build a business with real resilience. This guide covers every proven strategy, step-by-step, so you can stop reacting and start running your finances with confidence.

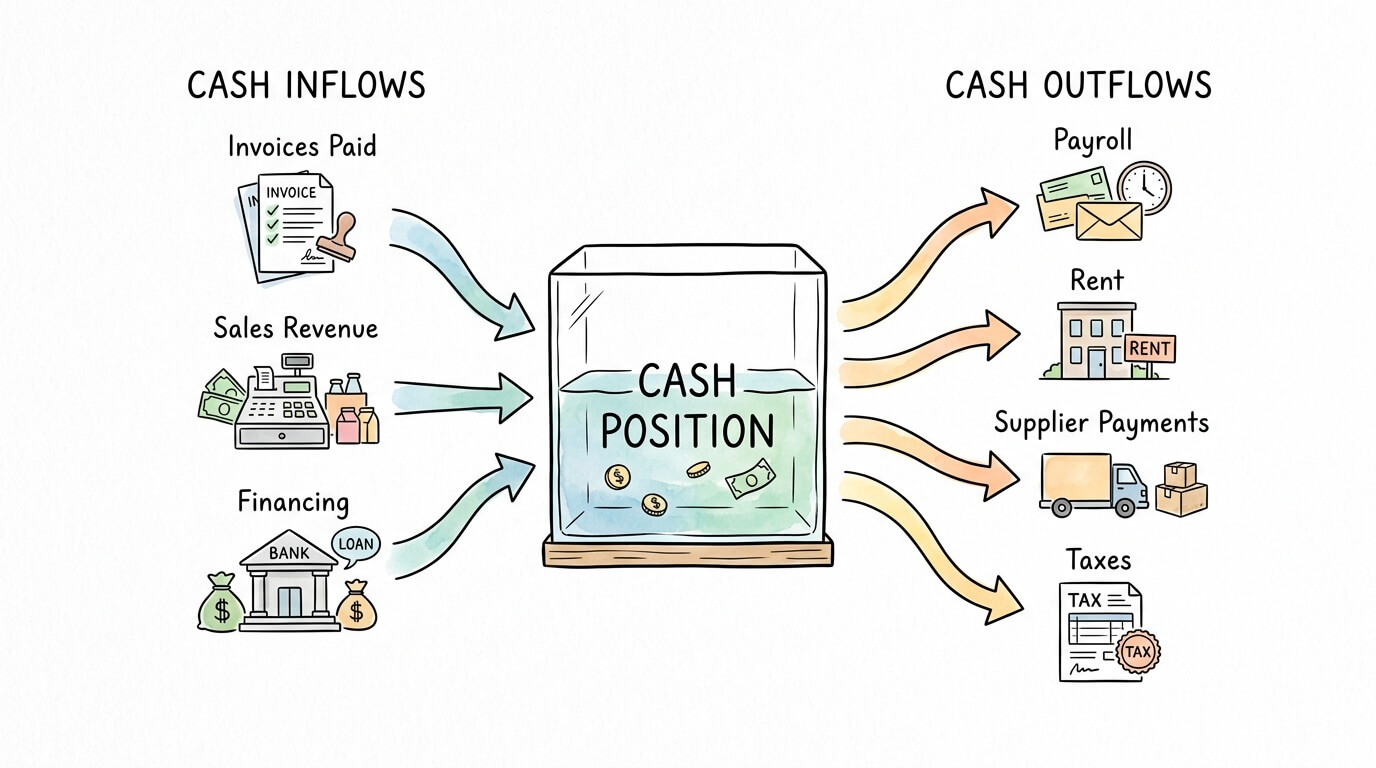

Improving cash flow means consistently ensuring more money enters your bank account than leaves it over any given period, and doing so predictably enough that you can plan ahead. It is not the same as being profitable.

Profit is an accounting concept. It lives on your income statement and tells you whether revenue exceeded expenses over a set period. Cash flow is visceral and real: it is the actual money in your accounts that you can use to pay rent, meet payroll, or invest in growth. A business can show strong profit on paper and still default on payroll if its clients pay on 90-day terms.

Pro Tip: Think of profit as your destination and cash flow as the fuel. You can have a perfect route planned, but if the tank runs dry, the journey stops.

The core formula is straightforward: Cash Inflows (payments received) minus Cash Outflows (payments made) = Net Cash Flow. Positive net cash flow means you have more coming in than going out. Negative means you are burning reserves. The goal is to make positive cash flow not just the norm, but a predictable constant.

Most business owners assume cash flow problems only happen to struggling companies. The reality is far more nuanced.

Seasonal revenue cycles create natural peaks and valleys. A landscaping company may generate 70% of its revenue between April and September, but payroll and rent continue every month. Extended payment terms are another silent culprit. B2B businesses routinely invoice on NET 30, NET 45, or even NET 60 terms, creating a structural gap between doing the work and getting paid.

The numbers are sobering. According to research from Intuit, 69% of small business owners have been kept awake at night worrying about cash flow. Meanwhile, the average small business carries about $53,399 in outstanding receivables at any given time, money already earned but not yet collected.

Understanding the root cause of your cash flow problem is the critical first step before choosing a solution.

| Root Cause | What It Looks Like | The Fix |

|---|---|---|

| Slow-paying clients | Outstanding invoices older than 30 days | Automate reminders; offer early payment discounts |

| Poorly structured payment terms | NET 60+ terms with no incentives for earlier payment | Renegotiate terms; implement dynamic discounting |

| No cash flow forecast | Surprises hit you instead of being anticipated | Build a rolling 12-week cash flow forecast |

| Uncontrolled variable expenses | "Miscellaneous" costs quietly grow month to month | Conduct a quarterly expense audit |

| Seasonal revenue gaps | Revenue dips in specific months, fixed costs do not | Build reserves during peak season; secure a credit line |

| Invoice errors and delays | Manual invoices go out late or with mistakes | Switch to automated invoicing software |

There is no single magic fix. The businesses that consistently maintain healthy cash flow layer multiple strategies together. Here are the six most effective approaches, ranked by speed of impact.

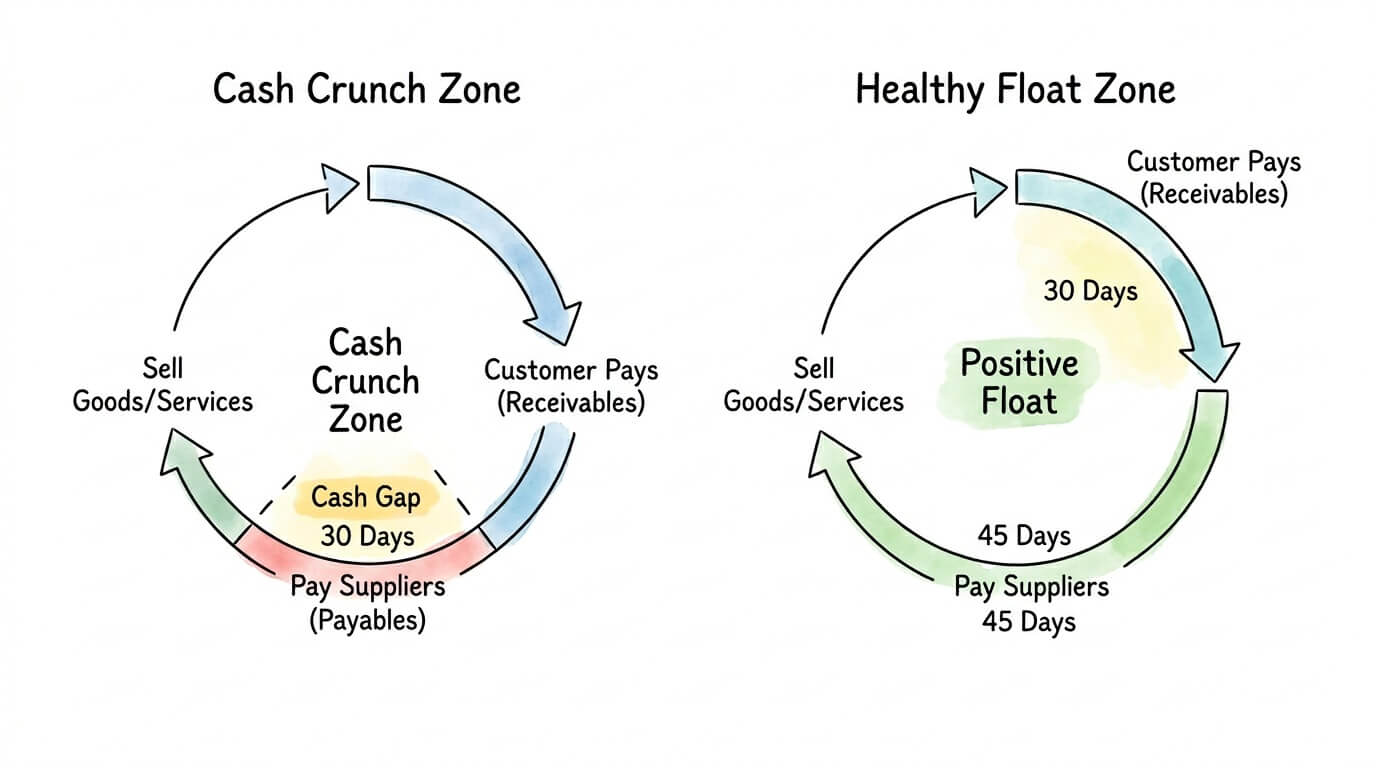

The fastest way to improve cash flow is to close the gap between doing the work and getting paid for it. Your accounts receivable (AR) represents money you have already earned. Every day it sits uncollected, you are essentially giving your clients an interest-free loan.

Send invoices immediately. The single most underrated tactic is timing. Every hour you delay sending an invoice is an hour you delay starting the payment clock. Businesses that invoice the same day work is completed get paid an average of 10 days faster than those who batch invoices weekly.

Optimize your invoice design. A confusing invoice creates questions, and questions create delays. Make sure every invoice includes: the exact amount due, the specific due date (not just "NET 30"), an itemized list of services, and at least two clear payment methods. The fewer reasons a client has to ask a question, the faster they pay.

Offer early payment discounts. A classic formula is "2/10 NET 30": the client gets a 2% discount if they pay within 10 days, otherwise the full amount is due in 30. For clients managing their own cash flow, this is a compelling incentive. For you, a 2% discount is far cheaper than financing the receivable through a line of credit.

Automate payment reminders. Manual follow-up on overdue invoices is time-consuming and awkward. Invoice automation tools can send polite, professional reminders at pre-set intervals (3 days before due, on the due date, and 7 days after) without any manual intervention. This alone can reduce your average Days Sales Outstanding (DSO) by 20-30%.

According to the AICPA, companies that switch to electronic invoicing report an average 17% reduction in DSO. That means if you are currently collecting in 45 days, you could be collecting in under 38 days just by going electronic.

Pro Tip: One study found that businesses accepting online payments get paid the same day in 57% of cases. Every payment method you remove is a direct tax on your cash flow speed.

If you are still creating, sending, and chasing invoices manually, you are not just losing time. You are introducing errors that directly delay payments. Research from IOFM (Institute of Finance and Management) shows that roughly 39% of manually processed invoices contain at least one error, and each error costs an average of $52 and 18 minutes of rework time.

Automating your invoicing workflow eliminates this entirely.

Modern invoice automation platforms like TallyScan connect directly to your email inbox and client portals, extract invoice data automatically using AI, and sync it directly to your accounting software. The result is a touchless invoice lifecycle: from receipt to reconciliation, with no manual data entry.

Here is what that transformation looks like in hard numbers:

| Metric | Manual Invoicing | Automated Invoicing | Improvement |

|---|---|---|---|

| Cost per invoice processed | ~$15.00 | ~$2.78 | -81% |

| Average processing time | 9.2 days | < 24 hours | -73% |

| Invoice error rate | ~39% | < 1% | -97% |

| DSO (Days Sales Outstanding) | 45+ days (avg) | ~37 days | -18% |

Source: IOFM 2025 Accounts Payable Benchmarking Survey

Beyond the direct cost savings, automation gives you something priceless: real-time visibility. You can see at a glance which invoices are outstanding, which are overdue, and which are at risk, without digging through spreadsheets or email threads.

To understand the full scope of what automation can do for your operation, see our guide on automating accounts payable, our breakdown of invoice automation software benefits, and our comparison of invoice capture software options.

Running a business without a cash flow forecast is like navigating without GPS. You may know your destination, but you have no visibility on the obstacles ahead. A 12-week rolling cash flow forecast is the single most powerful planning tool available to a small business owner, and it requires nothing more than a spreadsheet to start.

Step 1: List your opening cash balance. How much money is actually in your bank accounts today? Use the real number, not the amount you expect to receive.

Step 2: Project all cash inflows. List every payment you realistically expect to receive, including outstanding invoices (with their likely payment dates, not just due dates), recurring contracts, and projected new sales based on your pipeline.

Step 3: Project all cash outflows. List every bill you will pay: payroll, rent, software subscriptions, supplier invoices, loan repayments, taxes, and any planned purchases.

Step 4: Calculate your rolling net position. Subtract outflows from inflows for each week. The resulting number shows you whether you are heading toward a surplus or a crunch, with enough lead time to act.

Step 5: Run "what if" scenarios. What happens if your largest client pays 30 days late? What if a supplier raises prices by 10%? Scenario modeling transforms your forecast from a passive ledger into an active planning tool.

| If Your Forecast Shows... | You Can Proactively... |

|---|---|

| Cash surplus in 6 weeks | Prepay supplier invoices for a discount, invest in growth, or build reserves |

| Cash crunch in 4 weeks | Aggressively chase overdue AR, defer non-essential expenses, or draw on a credit line |

| Consistent seasonal dips | Build cash reserves during peak months to cover the slow periods |

| Steady growth pattern | Identify the right timing to hire, invest in equipment, or expand |

The goal of forecasting is not precision. It is preparedness. Even a rough forecast that is 80% accurate will prevent more financial crises than no forecast at all. The U.S. Small Business Administration recommends maintaining a rolling 13-week cash flow forecast as a baseline cash management standard for any business. For a broader guide on optimizing the end-to-end invoice workflow that feeds your forecast data, see our guide on how to streamline invoice processing.

Improving cash flow does not always mean growing revenue. Sometimes the fastest path to healthier finances is reducing what flows out. An honest, thorough expense audit often reveals more savings than most business owners expect.

Conduct a quarterly expense audit. Pull every transaction from the past three months. Categorize each expense as either fixed (rent, payroll, essential software) or variable (marketing, freelance, subscriptions). Your variable expenses are where the opportunity lives.

Common findings in a typical audit:

Negotiate better vendor payment terms. Extending your payment terms from NET 30 to NET 45 or NET 60 with key suppliers gives you an additional 15-30 days to use your cash. The math is simple but powerful: if you pay $50,000 per month to suppliers, shifting to NET 60 terms frees up $100,000 in working capital at any given time.

The key to successful term negotiation is framing it as a partnership conversation, not a demand:

"We have been a reliable partner for [X] years with a consistent payment history. As we align our payables with our revenue cycle, moving to NET 60 terms would help us plan more effectively and continue growing our relationship. Would you be open to discussing this?"

Cut waste, not capability. The goal is to remove spending that does not generate value, not to cut spending that drives growth. A poorly timed cost cut in marketing or talent can cost more in lost revenue than the savings generated.

For a deeper framework on managing the payables side, see our guide on accounts payable automation best practices and our guide on tracking accounts payable KPIs and dashboards.

Days Sales Outstanding (DSO) measures the average number of days it takes to collect payment after a sale. A high DSO is a direct drain on your cash position. Reducing it is one of the most impactful levers for improving cash flow in a B2B business.

The formula is: DSO = (Accounts Receivable / Total Credit Sales) x Number of Days

If your DSO is 55 and your revenue is $1 million annually, every 10-day reduction in DSO frees up approximately $27,000 in working capital. That is real money.

Tactics to reduce DSO:

According to the Atradius Payment Practices Barometer, late payments are cited as a top cash flow risk by 40% of B2B businesses globally, with actual payment delays extending an average of 15 days beyond agreed terms across many industries. For a complete system to monitor both your incoming and outgoing invoices in real time, see our guide on the best way to track invoices.

Even the best-run businesses encounter cash flow gaps. A key client pays late, a large expense hits unexpectedly, or a growth opportunity requires capital before revenue arrives. Smart financing is not a failure: it is a tool, and using it strategically is what separates resilient businesses from fragile ones.

Business Line of Credit. The most flexible option for ongoing cash flow management. A line of credit works like a high-limit business credit card: you draw what you need, pay interest only on what you use, and repay as cash comes in. It is ideal as a buffer for seasonal dips or unexpected expenses.

Invoice Factoring. If your primary problem is slow-paying B2B clients, invoice factoring converts your outstanding invoices into immediate cash. You sell the invoice to a factoring company at a small discount (typically 1-5%) and receive 80-95% of the face value immediately. The factoring company then collects directly from your client.

Revenue-Based Financing. For SaaS or subscription businesses with predictable recurring revenue, revenue-based financing provides a lump sum in exchange for a percentage of future monthly revenue until the advance is repaid. It scales with your business and requires no fixed monthly payment.

Merchant Cash Advance (MCA). Best suited for retail or restaurant businesses with high daily card transaction volume. An MCA provides upfront capital in exchange for a percentage of future daily card sales. Repayment is automatic and proportional to revenue.

| Financing Option | Best For | Main Advantage | Watch Out For |

|---|---|---|---|

| Business Line of Credit | Ongoing liquidity buffer for any business | Flexible; interest only on what you draw | Requires good credit history |

| Invoice Factoring | B2B businesses with slow-paying clients | Turns AR into same-day cash | Fees can range from 1-5% per invoice |

| Revenue-Based Financing | SaaS / subscription businesses | Repayment scales with revenue | Total repayment can be 1.2-1.5x the advance |

| Merchant Cash Advance | Retail / restaurants with high card volume | Very fast approval; no fixed payment | Effective APR can be very high |

Key Insight: Do not optimize for the lowest interest rate in isolation. Speed and flexibility are often more valuable. A credit line you can draw in 24 hours may deliver more ROI than a cheaper loan that takes three weeks to fund.

Use this diagnostic table to identify which areas of your business are most at risk. Score each row honestly to prioritize where to focus first.

| Area | Healthy Signs | Warning Signs | Your Score (1-5) | Priority |

|---|---|---|---|---|

| Invoicing speed | Invoices sent same day work is completed | Invoices batched weekly or monthly | — | High |

| Payment methods | 3+ payment options including online/ACH | Check only or single method | — | High |

| DSO (Days Sales Outstanding) | Under 35 days | Over 45 days | — | High |

| Cash flow forecasting | Rolling 12-week forecast updated weekly | No formal forecast process | — | High |

| Expense visibility | Monthly audit of all variable expenses | No categorized expense tracking | — | Medium |

| Vendor payment terms | NET 45 or better with key suppliers | NET 30 or less with all suppliers | — | Medium |

| Cash reserve | 60+ days of operating expenses in reserve | Less than 30 days in reserve | — | High |

| Financing readiness | Active credit line with available balance | No pre-established credit facility | — | Medium |

Scoring Guide: A score of 4-5 means healthy. A score of 1-2 means this area needs immediate attention. Total your scores: 32-40 is excellent; 20-31 needs work; below 20 is urgent.

The fastest way to improve cash flow is to accelerate collections on existing receivables. Start by sending any outstanding invoices immediately, offer a 2% early payment discount for payment within 10 days, and set up automated payment reminders. Additionally, contact your top 3-5 clients directly and ask about any outstanding invoices. These actions can convert existing AR into cash within days, without waiting for new sales.

Yes, absolutely, and this is one of the most dangerous traps in business. Profit is an accounting measurement of revenue minus expenses over a period. Cash flow is the actual money in your bank account. A business can have a highly profitable quarter on paper while simultaneously being unable to make payroll if clients have 90-day payment terms and no cash has actually arrived. This disconnect is why managing cash flow is essential for survival, while profit is the goal for long-term growth.

Invoice automation improves cash flow in three direct ways. First, it eliminates processing delays: automated invoices go out the moment a trigger occurs (job completion, contract milestone) rather than waiting for a manual billing cycle. Second, it reduces errors: automated systems have error rates below 1%, versus roughly 39% for manual processing, meaning fewer payment disputes and delays. Third, automated dunning sequences ensure reminders go out on schedule without requiring human follow-up, reducing average DSO by 17-30%.

For most small businesses, NET 15 or NET 30 is the optimal starting point, combined with a 2/10 early payment discount (2% off if paid within 10 days). For project-based work, requiring a 25-50% upfront deposit significantly reduces your AR exposure. Avoid NET 60+ terms unless you are dealing with enterprise clients where it is industry-standard and you have adequate cash reserves to bridge the gap.

To reduce DSO, focus on four tactics: send invoices immediately upon completing work; offer early payment discounts; automate your payment reminder sequence; and make it as easy as possible to pay (multiple payment methods, online portal access). Each of these tactics independently reduces DSO by 3-8 days. Combined, businesses commonly achieve DSO reductions of 15-20 days within 90 days of implementation.

For most small businesses, a weekly cash flow review is the right cadence. A weekly check-in lets you spot issues while there is still time to act. If your business is in a growth phase, navigating a cash crunch, or has irregular revenue cycles, daily monitoring during critical periods is warranted. At a minimum, complete a detailed monthly review comparing actuals against your forecast to recalibrate your projections.

A budget is a plan of how you intend to allocate resources over a future period (usually a year), based on targets and goals. A cash flow forecast is a rolling projection of the actual money you expect to receive and pay out over the next 4-13 weeks, based on real invoices, contracts, and known expenses. Budgeting is strategic; forecasting is operational. Both are essential, but for day-to-day liquidity management, the rolling cash flow forecast is the more immediately actionable tool.

Improving cash flow is not a one-time project. It is a set of systems, habits, and tools that compound over time. Start with the highest-impact lever for your current situation: if your DSO is above 45 days, focus on AR acceleration and invoice automation first. If your expenses are uncontrolled, run a thorough audit. If you are flying blind without a forecast, build one this week.

The businesses that consistently outperform their competition on cash flow do not do anything exotic. They send invoices faster, follow up more systematically, plan further ahead, and use the right financing tools at the right time.

If manual invoicing is your biggest bottleneck, TallyScan can automate your entire invoice workflow, from inbox extraction to accounting sync, eliminating the manual work that delays your cash. Explore how AI-powered invoice extraction can cut your processing time by up to 73% and get you paid faster, every cycle.

Ready to see it in action? Start your free trial of TallyScan today and take the first step toward a cash flow system that works for you, not against you.

10 automated invoice capture tools compared honestly. Includes real cost data, ROI calculator, format support matrix, and an 8-point evaluation checklist.

Manual AP costs $10-$15 per invoice. This guide maps where your process breaks down, the seven fixes with the best ROI, and the KPIs to track real improvement.