Insights

Automated Invoice Capture Software: 10 Tools Compared, Honestly Rated

10 automated invoice capture tools compared honestly. Includes real cost data, ROI calculator, format support matrix, and an 8-point evaluation checklist.

TallyScan Team

The audit notice arrives. Your stomach drops. You open the letter, scan the timeline, and immediately start mentally cataloging everything that is not in order. Sound familiar?

Here is the reframe that experienced finance teams operate from: an audit is not a judgment. It is a scheduled review. And like any scheduled review, the outcome depends almost entirely on how well you prepare, not on how clean your books happen to be on the day the auditors walk in.

Organizations that approach audit preparation proactively, starting weeks or months before the audit period begins, consistently experience shorter fieldwork windows, fewer findings, lower audit fees, and stronger relationships with their auditors. Organizations that scramble at the last minute consistently experience the opposite. This guide gives you the exact framework, timeline, and checklists the prepared organizations use.

The word "audit" covers very different processes. Your preparation strategy should match the specific type you are facing.

| Audit Type | Who Conducts It | Primary Focus | Typical Trigger |

|---|---|---|---|

| External Financial Audit | Licensed CPA firm | Financial statement accuracy, GAAP compliance | Annual obligation, investor requirement, lender covenant |

| IRS Tax Audit | Internal Revenue Service | Tax return accuracy, substantiation of deductions | Random selection, income discrepancy, industry flag |

| Internal Audit | Your own internal audit team | Operational efficiency, risk management, control effectiveness | Scheduled program, specific concern, regulatory requirement |

| Industry/Regulatory Audit | Government body or regulator | Industry-specific compliance (HIPAA, SOX, PCI-DSS, etc.) | Regulatory cycle, complaint, licensing renewal |

| Sales Tax Audit | State department of revenue | Sales tax collection and remittance accuracy | Nexus trigger, revenue threshold, industry flag |

Each type has different document requirements, different standards, and different auditor objectives. This guide focuses primarily on external financial audits and IRS tax audits, which are the most common for small and mid-size businesses, with notes on where the other types diverge.

Pro Tip: Read your audit engagement letter carefully before doing anything else. It specifies the audit type, scope period, applicable standards, and what the auditors need from you. Every preparation decision flows from that document.

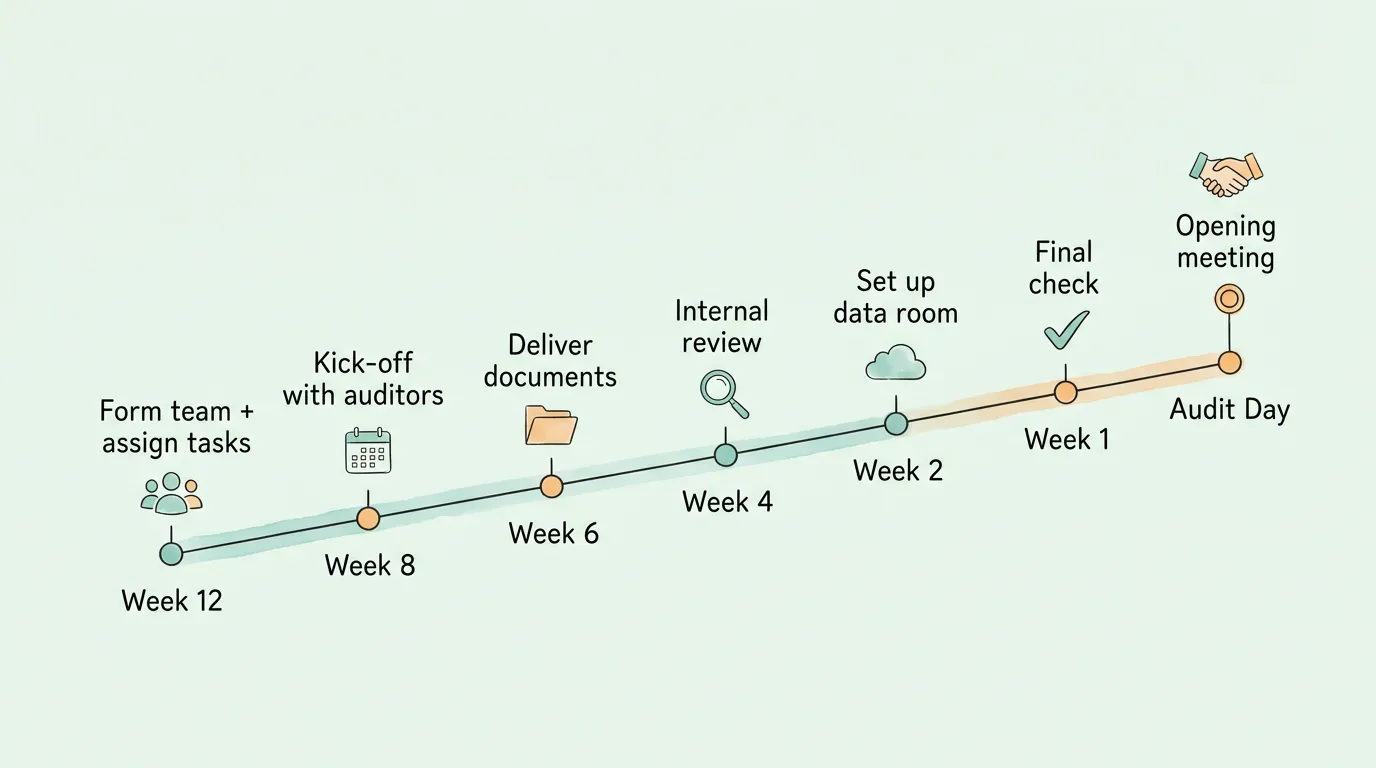

Most businesses think of audit preparation as something that starts when the auditors arrive. Best-in-class organizations start 12 weeks out. Here is the week-by-week roadmap.

| Timeframe | Priority Actions |

|---|---|

| 12 weeks before | Confirm audit dates; assign internal audit liaison; distribute self-assessment to all departments |

| 10 weeks before | Complete self-assessment; identify highest-risk control gaps; begin document collection |

| 8 weeks before | Hold kick-off call with audit firm; clarify scope and any significant accounting matters |

| 6 weeks before | Deliver preliminary PBC (Provided by Client) document list; complete financial reconciliations |

| 4 weeks before | Internal review of all collected documents using the four-eyes principle; prepare explanations for anomalies |

| 2 weeks before | Set up secure data room (physical or virtual); confirm system access for audit team |

| 1 week before | Final document check; brief all department contacts on their role and response protocols |

| Audit day 1 | Host opening meeting; introduce key contacts; walk auditors through any material changes since prior year |

Research from audit management firms shows that organizations with a formal pre-audit coordination process reduce on-site fieldwork time by up to 25%, directly reducing audit fees and internal disruption.

An audit is never a one-person job, and treating it as one is one of the most common mistakes. Your internal audit team needs to cover every area the auditors will examine.

Who should be on the team:

The SPOC role is critical. When auditors have a single, empowered contact who can retrieve documents quickly and answer questions accurately, fieldwork moves 30 to 50% faster than when requests are routed through multiple people who then route to other people.

Your team's first meeting should produce three outputs:

When an auditor requests a document and you produce it in under two minutes, you communicate something powerful: this organization is in control of its own records. When you say "I'll have to find that," you communicate the opposite.

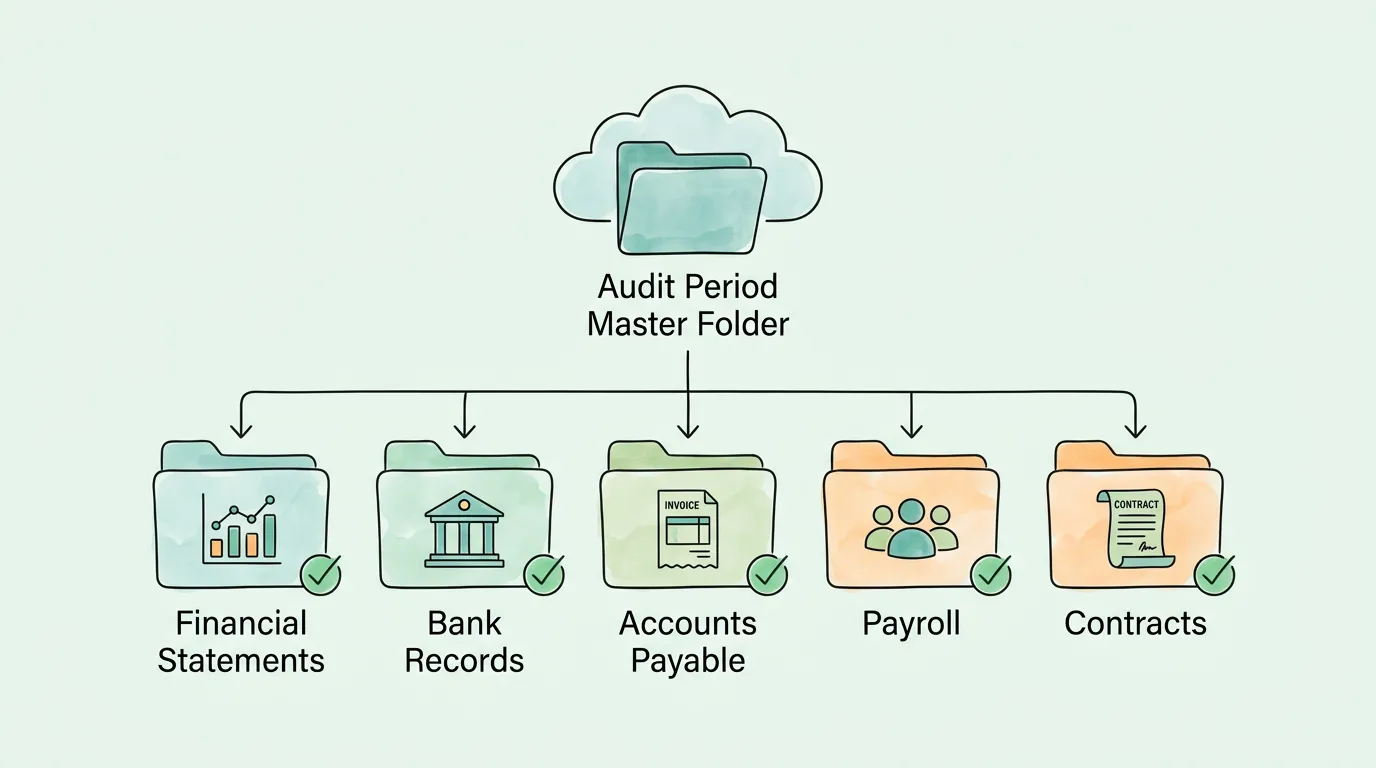

Build a digital command center. Create a structured folder hierarchy for the audit period, organized the way auditors think, not the way your filing system evolved:

[Audit Period] Master Folder

├── Financial Statements (monthly, quarterly, annual)

├── Bank Records

│ ├── Statements

│ └── Reconciliations

├── Accounts Receivable

│ ├── Sales Invoices

│ ├── Customer Contracts

│ └── AR Aging Reports

├── Accounts Payable

│ ├── Vendor Invoices

│ ├── Purchase Orders

│ └── Payment Records

├── Payroll

│ ├── Payroll Registers

│ └── Tax Filings (941, W-2, etc.)

├── Fixed Assets

│ ├── Asset Register

│ └── Depreciation Schedules

└── Contracts and Agreements

Use a master document tracker. A spreadsheet is sufficient. Columns should include: Document Category, Item Description, Period, Assigned To, Status (Not Started / In Progress / Collected / Reviewed), Location, and Notes/Issues.

| Document Category | Item | Period | Owner | Status | Notes |

|---|---|---|---|---|---|

| Accounts Payable | All vendor invoices over $500 | FY 2025 | AP Manager | In Progress | 47 of 61 collected |

| Bank Statements | Main operating account | Jan-Dec 2025 | Controller | Reviewed | All reconciled |

| Payroll | Q3/Q4 941 filings | Jul-Dec 2025 | HR Director | Collected | Awaiting review |

Apply the four-eyes principle to every critical document. The person who prepared a document should not be the only one who reviews it before it goes to auditors. A second reviewer catches the small errors and inconsistencies that the preparer, now blind to them from familiarity, will miss. Errors found internally look like good internal controls. The same errors found by auditors raise questions about your control environment.

For guidance on organizing vendor invoices and AP documents specifically, see our guide on how to reconcile invoices and our accounts payable tracking guide.

Auditors perform reconciliations as part of their testing. If they find discrepancies that you have not found and addressed first, it signals weak internal controls and typically triggers expanded testing, meaning more time, more questions, and higher fees.

The essential pre-audit reconciliation list:

A mid-size company that implemented automated three-way matching and a standardized month-end close process reduced its average close time from 14 days to 6 days and dramatically reduced audit adjustments in subsequent years. For practical reconciliation techniques, see our bank reconciliation tips guide.

Auditors are not just checking your numbers. They are evaluating the systems and processes that produced those numbers. Weak controls cause them to expand their testing because they cannot trust that the numbers are reliable. Strong, documented, tested controls allow them to rely on your systems and reduce the work they need to do themselves.

Run a pre-audit self-assessment. Walk through each major financial process as if you were the auditor. Map the process, identify control points, and ask: what could go wrong here? Where is the risk of error or fraud highest?

Score each area: 3 = Strong (documented, tested, operating effectively), 1 = Moderate (exists but rarely tested or partially documented), 0 = Weak (absent or operating inconsistently).

| Control Area | Green (3) | Yellow (1) | Red (0) | Your Score |

|---|---|---|---|---|

| Invoice approval workflow | All invoices approved before payment, system-enforced | Approval required but via email only | Invoices paid without documented approval | |

| Segregation of duties | No one controls a transaction end-to-end | Most duties separated, some gaps | Same person authorizes and records payments | |

| Bank reconciliation | All accounts reconciled monthly within 5 days | Reconciled quarterly, items unresolved | No formal reconciliation process | |

| Access controls | User permissions reviewed quarterly, MFA enabled | Permissions rarely reviewed | Former employees retain system access | |

| Expense policy documentation | Written policy with defined limits, approval levels | Informal guidelines exist | No written expense policy | |

| Duplicate payment detection | System-level duplicate check before payment | Manual search before payment | No duplicate detection process | |

| Document retention | 7-year digital archive, searchable, backed up | Mixed digital and paper | Paper only or no formal retention policy |

Scoring guide: 18-21 is strong. 10-17 has addressable gaps. Below 10 is high-risk and requires immediate action before the audit begins.

The most common control gaps, and how to close them:

Missing invoice approvals. If invoices are being paid without documented sign-off, establish a formal approval workflow immediately. Even a structured email chain with clear approval language is better than nothing. For vendor invoices, automated three-way matching (purchase order + goods receipt + invoice) is the gold standard for preventing unauthorized payments. See our invoice matching process guide for implementation detail.

Stale bank reconciliations. Bank accounts must be reconciled every month, without exception. A bank rec that is more than 30 days old when the audit begins is an immediate red flag.

Weak user access controls. Every user should have access only to the systems and data required for their specific role (principle of least privilege). Review user permissions quarterly and remove access for departing employees immediately, not at the next quarterly review.

No formal expense policy. An unwritten policy cannot be verified by an auditor. Document approval thresholds, receipt requirements, submission deadlines, and prohibited expenses. One page is enough to start.

For building audit-ready controls on the AP side, our audit readiness checklist provides a complete 10-pillar framework that covers all major control areas auditors examine.

The scope of external financial audits has expanded significantly over the past decade. Understanding modern audit priorities helps you prepare the right documentation and avoid being caught off-guard by questions that feel unexpected.

The foundation never changes: your financial statements must be accurate, complete, consistently presented, and supported by documentation that auditors can independently verify. Every number on your balance sheet and income statement must trace back to a source document.

PCAOB audit standards have expanded scrutiny of IT systems and data controls, reflecting the reality that financial data now lives in cloud systems, APIs, and third-party platforms. Auditors increasingly ask for:

For businesses subject to SOX requirements (public companies) or lender covenants requiring audited controls, ICFR testing is a formal component of the audit. Auditors test whether controls are designed correctly and operating effectively. Evidence of control testing performed by your own team (internal control testing documentation) reduces the amount of external auditor testing required.

Revenue recognized in the wrong period is one of the most common audit findings. Auditors test whether revenue is recorded when performance obligations are satisfied (under ASC 606), not when cash is received or invoices are sent. Have your revenue recognition policy documented, applied consistently, and supported by contracts and delivery evidence.

Any transactions between the company and its owners, directors, or related entities receive heightened auditor scrutiny. These transactions must be disclosed, documented, and conducted at arm's length (or disclosed if not). Identify all related-party transactions before the audit and have complete documentation ready.

Understanding what actually happens during fieldwork reduces anxiety and helps you support the auditors effectively.

Opening meeting (Day 1): The audit team introduces themselves, reviews the scope, and discusses the fieldwork plan. This is when you introduce your internal team, confirm the document delivery process, and clarify the communication protocol.

Document request and review: Auditors will submit information requests (IRs or PBC lists) throughout fieldwork. Your SPOC receives these, routes them internally, and returns completed documents as quickly as possible. Delays in document delivery are the single biggest driver of extended audit timelines.

Walkthroughs: Auditors will ask staff to walk through specific processes (how an invoice is received, approved, and paid) to assess whether controls described in your documentation are actually being followed in practice. Brief your staff on these processes before fieldwork begins.

Testing: Auditors select samples from your records and verify them against source documents. They are not reviewing everything; they are testing whether your processes work as described.

Closing meeting: Auditors summarize their findings, proposed adjustments, and any control observations. This is your opportunity to provide additional information on anything they noted and to understand what will appear in the final report.

Pro Tip: Treat every auditor request as urgent, regardless of how minor it appears. Prompt, complete responses build trust and keep fieldwork on schedule. Slow or incomplete responses trigger follow-up questions and extend the engagement.

The audit report is not the end. It is feedback you should act on before the next cycle begins.

Management letter / control observations: Most external audits produce a management letter alongside the audit report, detailing control weaknesses and recommendations. For each finding:

Adjust your preparation timeline. Use this audit's experience to update your 12-week preparation calendar. Which document categories took longest to collect? Which reconciliations had the most open items? Which auditor questions caught your team unprepared? Build the answers into next year's process.

Update your technology stack. Many of the most common audit findings, including missing invoices, reconciliation gaps, manual entry errors, and incomplete audit trails, are preventable with the right tools. Automating invoice capture means every vendor invoice is captured, stored, and linked to an approval record automatically. See our guide on invoice capture software and how streamlining invoice processing builds the continuous, audit-ready workflow that makes next year's preparation significantly easier.

The most time-consuming parts of audit preparation, gathering documents, reconciling accounts, tracing transactions to source records, are all processes that technology can largely automate.

Invoice and receipt capture automation eliminates the document-gathering problem at its root. When every vendor invoice is automatically captured from email, portals, and supplier systems, extracted using AI-powered OCR, and linked to its purchase order and payment record, the document trail that auditors need already exists. There is no hunting through email archives for a vendor invoice from eight months ago. For a technical overview of how this works, see our guide on what is OCR technology.

Bank reconciliation automation keeps your reconciliations current month-by-month rather than creating a catch-up project at audit time. Tools that connect directly to bank feeds and match transactions against your accounting records automatically flag unmatched items in real time.

AP automation with three-way matching creates the approval audit trail that auditors require. Every vendor invoice has a timestamped record of who received it, who approved it, what PO it matched against, and when payment was issued. This record exists automatically, without anyone needing to reconstruct it before the audit. For more on what a complete AP audit trail looks like, see our guide on invoice data capture software.

The Institute of Finance and Management (IOFM) reports that organizations using AP automation reduce audit preparation time by up to 70% compared to those using manual processes. The data trail is simply already there.

For a comprehensive framework of the controls and documentation that make organizations permanently audit-ready, see our audit readiness checklist and our audit preparation checklist.

For a scheduled external financial audit, start preparation 10 to 12 weeks before the audit fieldwork begins. This gives you time to complete financial reconciliations, identify and address control gaps, organize documentation, and brief your team without a last-minute scramble. For an unexpected IRS audit notice, start immediately: read the notice carefully to understand exactly what documents are being requested, gather only what is asked for (do not volunteer additional information), and consider engaging a CPA or tax attorney to represent you.

For an external financial audit, the standard document list includes: financial statements for the audit period, bank statements and reconciliations for all accounts, accounts receivable aging and supporting invoices, accounts payable aging and vendor invoices, payroll records and tax filings, fixed asset register and depreciation schedules, loan and debt agreements, significant contracts, and board or governance meeting minutes. Auditors will also request samples of specific transactions for detailed testing. Your audit engagement letter will include a preliminary PBC (Provided by Client) list specific to your situation.

Disorganization. Handing auditors a jumbled set of digital files, an email trail of documents with no index, or paper files in no particular order signals weak internal controls and almost guarantees they will expand their testing. A close second is waiting too long to start. Businesses that begin preparation six to eight weeks before the audit field date consistently have shorter, smoother audits than those that begin two weeks out. A third common mistake is letting auditors discover errors that the business already knew about. Disclosing known issues proactively, with a documented explanation and remediation plan, is always better than hoping auditors will not find them.

Yes, always. Proactive disclosure of an internally identified error, accompanied by a documented explanation of how it occurred and the steps taken to prevent recurrence, actually strengthens your position with auditors. It demonstrates that your internal controls are functioning: the system detected an error and corrected it. Auditors finding the same error independently raises a much larger question: why did your controls not catch it? The credibility cost of a discovered error far exceeds the credibility cost of a disclosed one.

Duration depends on company size, complexity, the quality of your preparation, and how responsive your team is to auditor requests. For small businesses (under $5 million in revenue), fieldwork often takes one to two weeks. For mid-market companies ($5 million to $100 million in revenue), two to four weeks is typical. For larger organizations or those with complex structures, fieldwork can extend to six weeks or more. The single biggest driver of extended timelines is slow document delivery. Organizations that pre-load their secure data room and respond to information requests within 24 hours consistently finish faster than average.

An external audit is conducted by an independent CPA firm, which expresses an opinion on whether your financial statements are presented fairly in accordance with accounting standards (GAAP or IFRS). The external auditor's opinion is for the benefit of shareholders, lenders, investors, and other third parties who rely on your financial statements. An internal audit is conducted by your own internal audit team (or co-sourced to a firm). Internal auditors report to your board or audit committee and evaluate the effectiveness of your risk management, controls, and operations. Internal audit findings are for management's benefit. Many organizations use internal audits as a preparation tool to identify and fix issues before external auditors arrive.

In accounts payable, auditors test for: completeness (are all obligations recorded?), cutoff accuracy (are expenses recorded in the correct period?), proper authorization (are all payments approved before being made?), and duplicate payments. They will sample vendor invoices and trace them back to purchase orders, goods receipts, and payment records. A complete, automated AP audit trail, where every invoice has a timestamped capture record, a matching record, an approval record, and a payment record, significantly reduces AP testing time. For an in-depth look at what strong AP documentation looks like, see our invoice matching process guide and our accounts payable tracking guide.

The IRS requires businesses to retain records supporting income and deductions for a minimum of 3 years from the filing date, with longer requirements for certain categories. For external financial audits, a 7-year digital retention policy is the standard conservative approach. Digitally organized expense records, with each receipt linked to its accounting entry, a business purpose note, and the original image, satisfy both IRS requirements and external auditor documentation standards. For a practical receipt organization system, see our guide on how to organize receipts for taxes.

The organizations that consistently have the smoothest audits are not necessarily the ones with the fewest problems in their books. They are the ones whose finance teams know where every document is, can explain every transaction, and have controls that visibly operate the way they are supposed to. That combination takes time and process discipline to build, but it is entirely achievable with the right framework and the right tools.

TallyScan automates the invoice and receipt capture workflow that creates your audit trail automatically: every document captured, every data field extracted, every approval timestamped, all synced directly to your accounting system. By the time auditors arrive, the documentation they need is already organized and retrievable in seconds.

Ready to make your next audit the smoothest one yet? Start your free trial of TallyScan today and build the audit-ready AP workflow that makes year-round compliance effortless.

10 automated invoice capture tools compared honestly. Includes real cost data, ROI calculator, format support matrix, and an 8-point evaluation checklist.

Manual AP costs $10-$15 per invoice. This guide maps where your process breaks down, the seven fixes with the best ROI, and the KPIs to track real improvement.