Insights

Automated Invoice Capture Software: 10 Tools Compared, Honestly Rated

10 automated invoice capture tools compared honestly. Includes real cost data, ROI calculator, format support matrix, and an 8-point evaluation checklist.

TallyScan Team

The month-end close is where financial reality meets financial reporting. Done well, it gives leadership a clear and trustworthy picture of the business. Done poorly, it produces numbers that look credible but do not actually reflect what happened — and those inaccuracies compound quietly until they surface at the worst possible time: during an audit, a fundraise, or a board meeting where someone asks a question the CFO cannot confidently answer.

A balance sheet reconciliation checklist is the structured process that closes the gap between those two outcomes. It is the systematic verification that every account on your balance sheet is supported by documentation, that the numbers match their source records, and that any differences are identified, explained, and resolved. Below you'll find all eight account categories broken down step by step: what to check, how often, and what the red flags look like, through to the automation layer that turns a multi-day scramble into a routine close.

A balance sheet reconciliation is the process of verifying that the balance reported in each account on the balance sheet matches the underlying transactions, sub-ledgers, or external statements that support it. For each account, you confirm that:

The goal is not just numerical accuracy — it is auditability. Every balance should be traceable to source documents that an auditor, a lender, or a tax authority could verify independently. When that traceability exists for every account, your financial statements are reliable. When it does not, you are reporting numbers you cannot fully defend.

Balance sheet reconciliation is different from bank reconciliation (which is one specific step within it) and different from a trial balance review (which checks that debits equal credits but does not verify that the individual balances are correct).

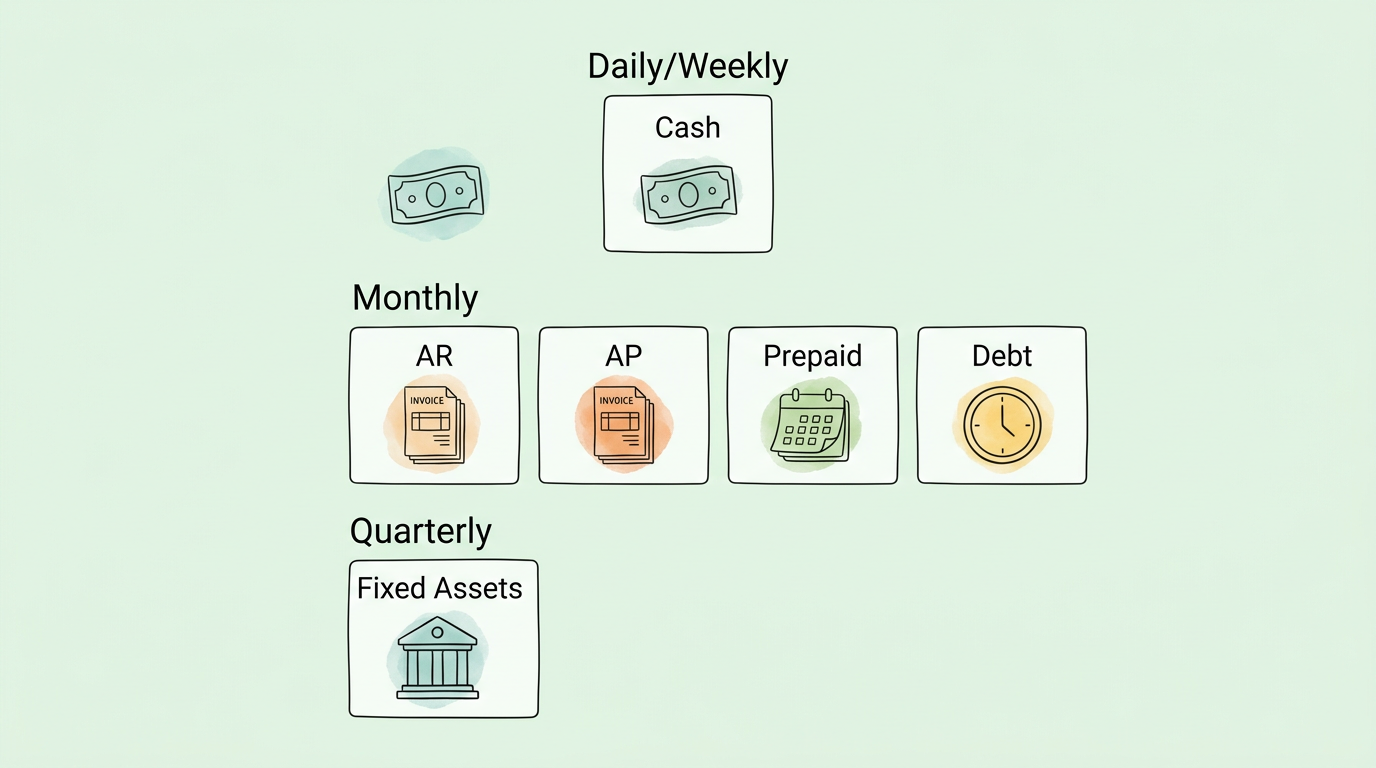

Not all balance sheet accounts carry equal risk or change with the same frequency. The reconciliation schedule should reflect both.

| Account Category | Recommended Frequency | Risk if Skipped |

|---|---|---|

| Cash and bank accounts | Daily or weekly | Fraud, overdraft, misappropriation |

| Accounts receivable | Monthly (aging weekly) | Overstated assets, bad debt underestimation |

| Prepaid expenses | Monthly | Misstated expenses, overstated assets |

| Inventory | Monthly (cycle counts) + annual full count | Shrinkage, valuation errors, COGS misstatement |

| Fixed assets | Quarterly physical audit + monthly depreciation | Ghost assets, wrong depreciation, tax errors |

| Accounts payable | Monthly | Understated liabilities, duplicate payments |

| Accrued liabilities | Monthly (period-end) | Incomplete expense recognition |

| Debt and interest | Monthly | Covenant violations, interest misstatement |

| Equity and retained earnings | Monthly | Shareholder reporting errors, compliance issues |

For businesses preparing audited financial statements, every account on the balance sheet requires formal monthly reconciliation. For smaller businesses, a tiered approach (daily for cash, monthly for most accounts, quarterly for fixed assets) achieves most of the benefit at a manageable workload.

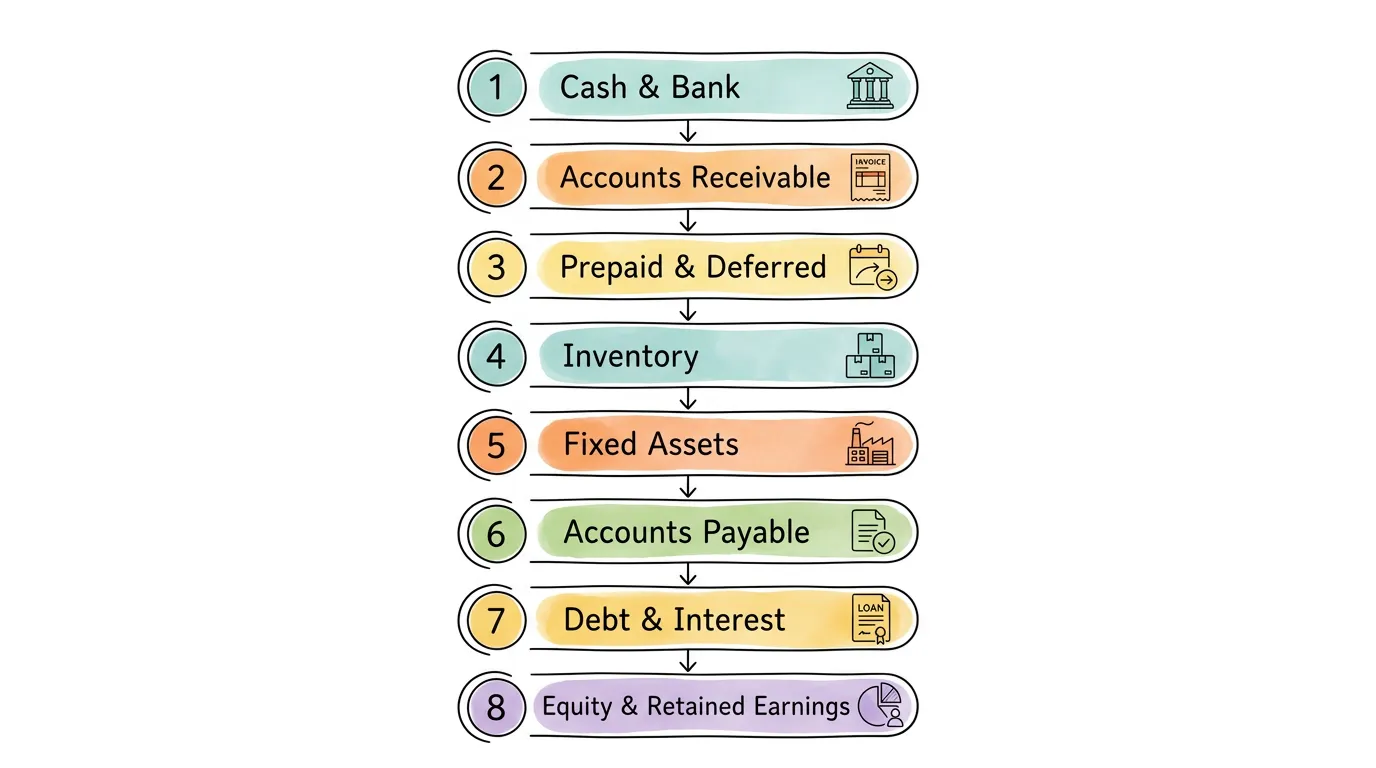

What it covers: All checking accounts, savings accounts, money market funds, petty cash, and restricted cash balances.

The reconciliation process:

Why it matters for the balance sheet: Cash is the most liquid asset and the most common target for fraud and misappropriation. An unreconciled cash balance means your reported liquidity is unreliable — which affects working capital calculations, covenant compliance checks, and lender confidence.

Key controls: Segregate the person who initiates payments from the person who reconciles the bank account. Reconciliation should be performed by someone who does not have access to initiate transactions.

For a detailed guide to making bank reconciliation faster and more reliable, see bank reconciliation tips.

Red flags to investigate immediately:

What it covers: All amounts owed by customers for goods or services delivered, plus the allowance for doubtful accounts.

The reconciliation process:

Why it matters for the balance sheet: AR is typically one of the largest current assets. Overstating it by carrying uncollectible balances inflates assets, overstates working capital, and misrepresents the quality of earnings. Under FASB ASC 310 guidance on receivables, the allowance for doubtful accounts must be estimated using a methodology that reflects expected credit losses.

Collection policy integration: The aging report should drive action, not just documentation. Every account in the 61-90 day bucket should have a documented collection action and a next-step date. Every account in the 90+ bucket should have a formal collectibility assessment and either an active collection effort or a write-off recommendation.

What it covers: Amounts paid in advance for services not yet received (prepaid insurance, prepaid subscriptions, prepaid rent) and amounts received from customers in advance of delivery (deferred revenue, customer deposits).

This step is commonly omitted from balance sheet reconciliation checklists. It is a significant source of misstatement because both accounts require active amortization that must be calculated and reviewed each period.

The reconciliation process for prepaid expenses:

The reconciliation process for deferred revenue:

Why it matters for the balance sheet: Prepaid expenses and deferred revenue directly affect both the balance sheet (asset and liability accuracy) and the income statement (expense and revenue timing). Errors here produce mismatched periods, where expenses and revenues that belong to different accounting periods are reported together.

What it covers: Raw materials, work-in-process, and finished goods. Applicable to any business that holds physical product.

The reconciliation process:

Cycle counting vs. annual count: For most businesses, a rolling cycle count program — counting a portion of inventory each week so that all items are counted at least once per quarter — provides more reliable inventory accuracy than a single annual physical count with minimal disruption to operations.

Why it matters for the balance sheet: Inventory is a direct input to cost of goods sold. Overvalued inventory overstates assets and understates COGS, inflating reported profit. Undervalued inventory has the opposite effect. Either error creates financial statements that do not accurately represent the business's performance or position.

What it covers: Property, plant, and equipment (PP&E) including land, buildings, vehicles, machinery, leasehold improvements, and capitalized software.

The reconciliation process:

Capitalization policy: Every business should have a documented capitalization threshold (typically $1,000–$5,000 depending on business size) that specifies when a purchase is capitalized as a fixed asset versus expensed immediately. Inconsistent application of this threshold is one of the most common fixed asset reconciliation errors.

Ghost assets: Assets recorded on the books that no longer physically exist (disposed of informally, lost, stolen) create phantom asset values that overstate total assets and accumulated depreciation. Annual or semi-annual physical verification of major asset categories is the primary control against ghost assets.

What it covers: Amounts owed to vendors for goods and services received but not yet paid, plus expenses incurred in the period but for which no invoice has yet been received.

This step is fundamentally different from the others because the risk is understatement rather than overstatement. You are looking for obligations that exist but have not been recorded.

The reconciliation process:

Three-way matching integration: The strongest control over AP accuracy is a three-way matching process — matching the purchase order, the goods receipt note, and the vendor invoice before any invoice is approved for payment. When this control is automated, most AP completeness issues are caught at entry rather than during reconciliation. For a guide to automating this process, see invoice matching process and improve accounts payable efficiency.

Why it matters for the balance sheet: Understated liabilities overstate equity and net income. This is one of the most common forms of financial misrepresentation — whether intentional or not — because the error is invisible until an invoice arrives or an auditor asks about goods receipts that were not matched to payables. For a full breakdown of the AP automation picture, see accounts payable automation best practices.

What it covers: All short-term and long-term borrowings including bank loans, lines of credit, equipment financing, convertible notes, and any other debt instruments.

The reconciliation process:

Covenant monitoring: Loan covenants are legal obligations. Breaching a covenant can trigger default provisions even if the loan payments are current. A debt reconciliation checklist should include a formal covenant compliance review at each month-end, not just at the annual audit. For businesses with multiple debt instruments, a dedicated debt management spreadsheet or software tool that tracks each covenant calculation automatically is worth the investment.

Why it matters for the balance sheet: Misstated debt affects leverage ratios, borrowing capacity, and lender relationships. Incorrect interest expense misrepresents the income statement. Incorrect current/long-term classification misleads users of the financial statements about the company's near-term obligations.

What it covers: Common stock, additional paid-in capital, treasury stock, accumulated other comprehensive income (AOCI), and retained earnings.

The reconciliation process:

Why it matters for the balance sheet: Equity represents the net worth of the business and the residual interest of shareholders. Errors in equity accounts affect EPS calculations for public companies, shareholder distributions, regulatory compliance, and future fundraising. For businesses preparing for a financing round or an acquisition, clean equity reconciliation is a due diligence requirement.

For guidance on building audit-ready records across all account categories, see audit readiness checklist and how to prepare for an audit.

| Account Category | Primary Risk | Key Data Source | Reconciling Items | Frequency |

|---|---|---|---|---|

| Cash and bank | Fraud, misappropriation | Bank statements | Outstanding checks, deposits in transit | Daily/weekly |

| Accounts receivable | Overstated assets | AR sub-ledger, aging report | Bad debt provision, credit memos | Monthly |

| Prepaid expenses | Period mismatement | Prepaid schedule | Amortization entries, expired prepaids | Monthly |

| Inventory | COGS misstatement | Perpetual system, physical count | Shrinkage, obsolescence, WIP valuation | Monthly + cycle counts |

| Fixed assets | Ghost assets, wrong depreciation | Fixed asset register | Additions, disposals, impairment | Quarterly physical + monthly depreciation |

| Accounts payable | Understated liabilities | AP sub-ledger, vendor statements | Unmatched receipts, unrecorded invoices | Monthly |

| Accrued liabilities | Incomplete period recognition | Accrual schedule | Recurring accruals, prior period reversals | Monthly |

| Debt and interest | Misstated leverage | Loan statements, amortization schedules | Interest accrual, current/long-term split | Monthly |

| Equity | Shareholder reporting errors | Cap table, board minutes, option register | SBC expense, dividend declarations | Monthly |

These errors appear consistently across businesses of all sizes. Recognizing them helps you build controls before they become problems.

Reconciling only to internal records. Confirming that the GL matches the sub-ledger proves internal consistency — it does not prove accuracy. True reconciliation requires matching to an independent external source: bank statement, vendor statement, lender confirmation, or auditor-circularized confirmation. An internal reconciliation that shows no differences may simply mean the same error is in both systems.

Carrying unexplained reconciling items forward. A reconciling item that does not resolve within 30 days is a red flag. Carrying the same unknown difference from one period to the next is not reconciliation; it is postponement. Every reconciling item should have a documented explanation, an expected resolution date, and an owner responsible for resolution.

Inconsistent cut-off treatment. Whether revenue is recognized in December or January, whether the December utility accrual is posted, whether the December 31 invoice is AP in December or January — these decisions should be governed by documented policies applied consistently every period. Inconsistent cut-off treatment produces financial statements that are not comparable across periods.

Reconciling without reviewing. A reconciliation that confirms numbers match is necessary but not sufficient. Someone with financial judgment — not just the person who prepared the reconciliation — should review the output for reasonableness: Is the AR aging profile worsening? Is the cash balance consistent with expected cash flow? Is the prepaid schedule complete? Independent review catches errors that preparers overlook because they are too close to the work.

Not maintaining supporting documentation. A reconciliation that exists only in someone's memory, or in a format that cannot be retrieved during an audit, provides no assurance. Each reconciliation should produce a documented output — a reconciliation schedule, a tie-out sheet, or a system-generated report — that is stored and retrievable. For guidance on the document management practices that support this, see accounting document management.

Treating reconciliation as a month-end-only activity. When reconciliation happens only at month-end, the team is always catching up to a full period of transactions. Moving high-risk accounts (especially cash and AP) to weekly or continuous reconciliation reduces the volume of items to investigate at any one time and catches errors much closer to when they occurred.

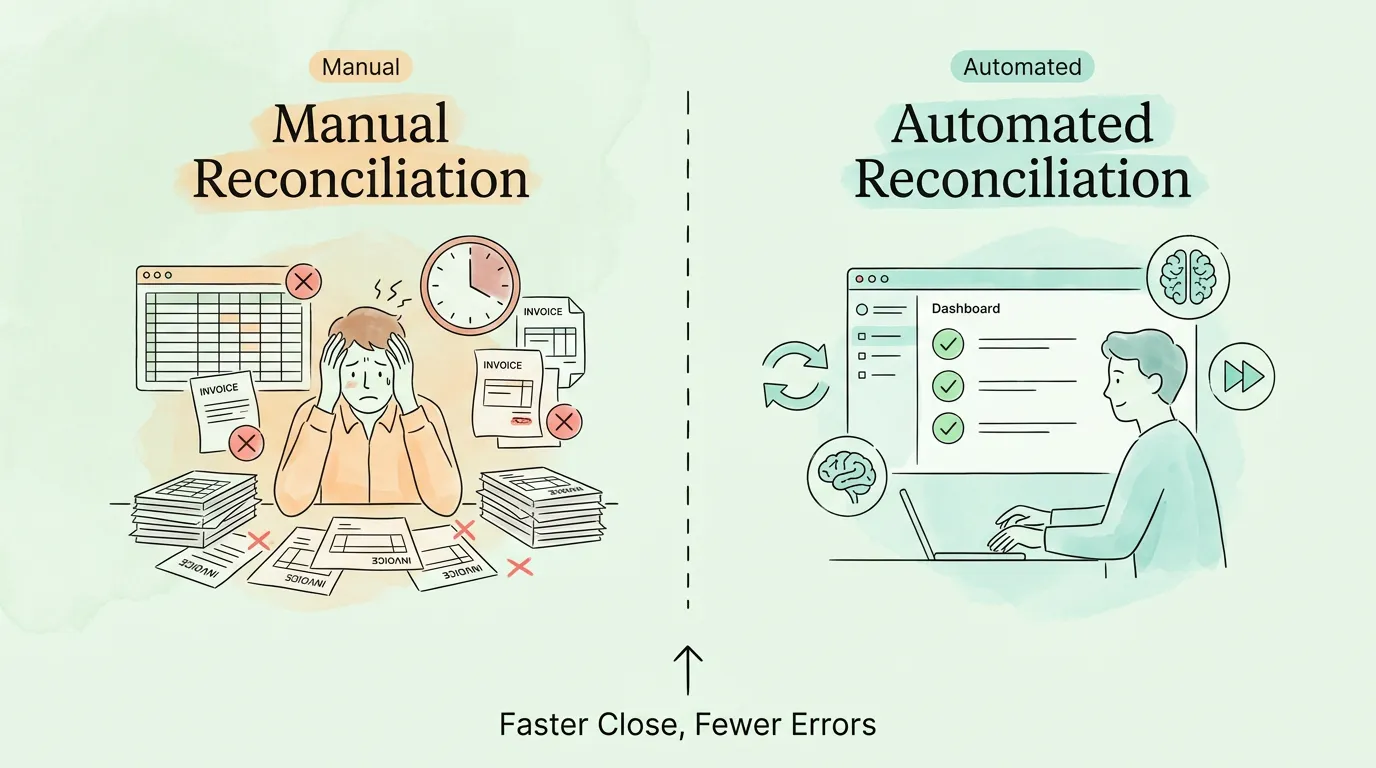

A manual balance sheet reconciliation checklist depends on each step being initiated, tracked, and completed by individuals. When someone is sick, overwhelmed, or simply forgets a step, the checklist breaks. Automation addresses the structural weakness: it eliminates the dependency on individual memory and manual coordination for the mechanical parts of the process.

The automation opportunities are different at each step:

Cash: Bank feed integration automatically imports transactions and suggests matches in near real-time. Instead of a once-a-month reconciliation of hundreds of transactions, the team reviews a daily exception list of unmatched items. See our guide on accounting automation software for what bank feed automation looks like in practice.

Accounts payable: Automated invoice capture (from email inboxes and vendor portals), AI-powered data extraction, and three-way matching logic eliminates most manual AP data entry and catches discrepancies before invoices are approved for payment. This dramatically reduces the AP completeness testing burden at month-end because the controls are operating continuously. For a detailed breakdown, see automate accounts payable.

Invoice and receipt reconciliation: AI-powered OCR captures every invoice and receipt automatically, extracts key fields, and matches them to purchase orders and bank transactions. The reconciliation work that used to happen manually at month-end happens continuously as documents arrive. See how to reconcile invoices for a practical guide to this process.

Depreciation and prepaid amortization: Accounting software with fixed asset modules and prepaid schedules calculates and posts these entries automatically each period, eliminating a significant category of manual journal entry work.

Reporting: Automated reconciliation platforms produce period-end reconciliation packs — standardized documentation for each account showing opening balance, movements, closing balance, and reconciling items — that can be reviewed and approved in the system rather than assembled manually from spreadsheets.

The result of automating the mechanical steps is that your finance team's month-end work shifts from data gathering and entry to review and analysis — the work that actually requires human judgment. For a broader look at how accounting process automation changes the finance function, see accounting process automation and accounting workflow management.

Rate your current process on each dimension from 1 (not in place) to 5 (fully implemented and consistently applied).

| Dimension | 1 — Not in place | 3 — Partial | 5 — Fully implemented | Your Score |

|---|---|---|---|---|

| Coverage | Several balance sheet accounts not reconciled | Most accounts reconciled; a few gaps | Every balance sheet account reconciled monthly | |

| External verification | Reconciliation is only internal (GL to sub-ledger) | Cash and AP verified externally; others internal only | All major accounts verified against external sources | |

| Documentation | Reconciliations exist in preparer's head or informal notes | Reconciliations documented but not standardized | Standardized reconciliation packs for each account | |

| Independent review | Preparer reviews their own work | Senior reviews some accounts | All reconciliations reviewed by someone other than preparer | |

| Cut-off consistency | Inconsistent; varies by preparer | Documented policy; not always applied | Consistent cut-off policy applied every period | |

| Timely resolution of items | Items carried forward without resolution | Most items resolved within 60 days | All items resolved within 30 days or escalated | |

| Automation | Fully manual | Bank feeds automated; rest manual | Most repetitive steps automated | |

| Close timeline | Month-end close takes 10+ business days | 5–8 business days | Under 5 business days |

Score interpretation:

A balance sheet reconciliation checklist is a structured list of verification steps that confirm every account on the balance sheet is accurate, complete, and supported by documentation. It covers all asset, liability, and equity accounts — from cash and accounts receivable to debt, accrued liabilities, and retained earnings. The checklist ensures that the closing balance in each account matches its corresponding external record (bank statement, vendor statement, loan amortization, physical count), that timing differences are identified and documented, and that any discrepancies are investigated and resolved before financial statements are issued.

The recommended frequency depends on the account and the business's risk profile. Cash accounts should be reconciled daily or weekly given the fraud and liquidity risk. Accounts receivable, accounts payable, accrued liabilities, debt, and equity should be reconciled monthly as part of the month-end close. Inventory should be reconciled monthly using a perpetual system, with cycle counts covering all items at least once per quarter. Fixed assets require monthly depreciation validation and at least an annual physical verification of major asset categories. For businesses preparing audited financial statements, all accounts require formal monthly reconciliation.

Bank reconciliation is one specific step within balance sheet reconciliation. It verifies the cash and bank account balances specifically, matching the GL balance to the bank statement and explaining differences like outstanding checks and deposits in transit. Balance sheet reconciliation is the broader process that covers all accounts on the balance sheet — cash, receivables, prepaid expenses, inventory, fixed assets, payables, accrued liabilities, debt, and equity. A complete balance sheet reconciliation includes bank reconciliation as its first step.

The most common errors are: (1) reconciling only to internal records rather than external sources, which confirms consistency but not accuracy; (2) carrying unexplained reconciling items forward from period to period without investigation; (3) inconsistent cut-off treatment, where the same type of transaction is handled differently in different periods; (4) the preparer reviewing their own reconciliation without independent review; (5) inadequate allowance for doubtful accounts that overstates AR; (6) unrecorded accrued liabilities that understate expenses and obligations; and (7) misclassification of debt between current and long-term.

For a small business with straightforward transactions and good automation, a complete month-end close including all reconciliations should take two to four business days. For a mid-size company with more complex accounts, five to seven business days is typical. For large enterprises, three to five business days is achievable with good workflow and automation. The main drivers of a slow close are: manual data gathering (solved by bank feeds and automated invoice capture), lack of standardized reconciliation templates (solved by documented processes), and sequential rather than parallel work (solved by assigning account ownership so multiple accounts are reconciled simultaneously).

Automation improves reconciliation in three ways. First, it eliminates manual data entry — bank feeds, automated invoice capture, and direct API connections to vendor systems mean data is already in the accounting system rather than being keyed in. This removes the most error-prone step. Second, it accelerates matching — automated three-way matching, bank transaction matching, and AR payment application happen in real time rather than at month-end, so the reconciliation workload is distributed across the month rather than concentrated in the last three days. Third, it produces standardized documentation — reconciliation packs, exception reports, and audit trails are generated by the system rather than assembled manually from spreadsheets. For a practical overview of the tools involved, see accounting automation software.

For each account reconciled, you should retain: the reconciliation schedule showing opening balance, period transactions, closing balance, and reconciling items; the external source document (bank statement, vendor statement, loan confirmation) that was matched against; a log of all reconciling items with their explanations and expected resolution dates; evidence of independent review (reviewer signature or system approval log); and the journal entries that resulted from the reconciliation. This documentation should be stored in an organized, retrievable format — not in individual spreadsheets on personal desktops. Retention periods should follow your jurisdiction's requirements; in the US, financial records supporting tax filings should generally be retained for seven years per IRS guidance on record retention.

A balance sheet reconciliation checklist is not the goal — financial accuracy is. The checklist is the mechanism that reliably produces that accuracy period after period, regardless of who is doing the work or how busy the period was.

The finance teams that close fastest and with the fewest errors are not the ones who work harder at month-end. They are the ones who have built systems — standardized templates, clear account ownership, automated data capture, consistent cut-off policies, and independent review — that make accurate reconciliation the path of least resistance. Month-end becomes a review and sign-off on work that has been happening continuously, not a scramble to reconstruct what occurred.

TallyScan automates the invoice and receipt capture that feeds your AP reconciliation — pulling documents from email and vendor portals, extracting key fields with AI-powered OCR, matching to purchase orders, and syncing approved data to your accounting platform. The AP side of your balance sheet reconciliation stays current without manual data entry.

Start your free trial and close your books faster.

Related reading: Bank Reconciliation Tips | Accounts Payable Automation Best Practices | Invoice Matching Process | Audit Readiness Checklist | How to Prepare for an Audit | Accounting Automation Software | Accounting Process Automation

10 automated invoice capture tools compared honestly. Includes real cost data, ROI calculator, format support matrix, and an 8-point evaluation checklist.

Manual AP costs $10-$15 per invoice. This guide maps where your process breaks down, the seven fixes with the best ROI, and the KPIs to track real improvement.